Beyond Traditional Stock Options: The Strategic Advantage of Stock Appreciation Rights (SARs)

In today's fiercely competitive business landscape, where building a successful company is just the beginning, the race to attract and retain top-tier talent has become a global strategic imperative. With a staggering 1,12,718 startups in India (as of October 2023) and the global workforce expanding rapidly, structuring innovative employee incentive plans has taken centre stage.

The on set of the pandemic in 2020 triggered a surge in companies offering employee incentive plans to conserve cash during revenue downturns and retain valuable talent.

Let us explore an often lesser-known employee incentive plans known as Stock Appreciation Rights (SARs), which has been gaining popularity recently. This could be a valuable option for startups to contemplate, offering a flexible framework that benefits both employers and employees in terms of incentivisation. It can assist in evaluating choices and crafting an employee incentive plan that aligns with your startup's vision and goals.

1. What are Stock Appreciation Rights (SARs)?

- A Stock Appreciation Right (SAR) is an employee incentive plan that allows employees to gain from the ‘appreciation’ in the value of a startup or company's shares beyond a predetermined exercise price or threshold value.

- This payout can be settled either in the form of shares or cash.

2. What are the modes of settlement for SARs?

SARs can be settled in three ways:

- Equity settled SAR.

- Cash settled SAR.

- Combination of equity settled, and cash settled SAR.

The mode of settlement will be determined upfront at the time of grant.

3. What factors could lead a company to opt for SARs?

- Equity preservation: SARs offer a share in company’s growth in value without dilution of equity at the time of grant.

- Customisable conditions: SARs may have time or performance-based conditions that can be tailored for various employee levels.

- Retention and value growth: Encourage employee retention and contribution to company value growth.

- Financial ease: SARs eliminate the need for cash outlay (exercise price) upon exercise, reducing financial burden on employees compared to stock options.

- Flexible Settlement Options: SARs offer the choice of cash or equivalent shares settlement, allowing companies to align incentives with their financial strategies and stakeholder interests.

4. How is the value of the SARs determined?

- SARs function by granting employees the opportunity to benefit from an increase in the estimated value of the company's shares over a specified time frame.

- This increase in value is determined by calculating the difference between the stock price at the time of grant and the stock price at the time of exercise, expressed as:

Appreciation = Fair Market Value on exercise date (minus) Base price on grant date.

- At the time of exercise, the employee will be rewarded with:

- Equity shares allotment to the extent of value appreciation; and/or

- Cash equal to the value appreciation.

Case Study: Employee Benefits from SARs at Jupiter

Jupiter, India’s largest consumer-focused digital fintech platform, had adopted Stock Appreciation Rights (SARs) to reward its employees amidst rapid company growth and significant fundraising. In January 2020, its valuation from INR 430 crore to INR 720 crore which helped the employees see value.

This strategic move involved granting 24,386 SARs to employees, a decision reflecting the company's recognition of its workforce's contributions. Unlike traditional stock options, SARs offer employees a bonus equivalent to the increase in the company's share value over time, without necessitating any personal investment.

Illustrative Example: If an employee was granted 100 SARs during the initial valuation (INR 430 crore), post the new round:

- Share price would increase from INR 24,531.17 to INR 36,095.76 per share.

- The value of SARs increased from Rs 22.53 lakhs to Rs 36 lakhs.

- This resulted in a net gain of Rs 13.56 lakhs for such employee, settled in either in cash or equity shares at the time of exercise.

This case highlights the benefits of SARs in fostering employee loyalty and motivation, aligning their interests with the company’s success, and creating a sense of ownership and partnership in the organisation's growth journey.

5. Is there a minimum vesting period for SARs?

- While there are no specific regulations covering this for a startup/private company, the general practice is to adopt the rules and procedures that are applicable to ESOPs, such as a minimum vesting period of 1 year between the grant of options, vesting of options, and adoption of Policy in accordance with Rule 12 (6) (a) of Companies (Share Capital and Debentures) Rules, 2014.

- From a startup's perspective, a 12-month vesting period is essential to encourage employees to dedicate their efforts to company’s growth and provide an opportunity for the accumulation of value over time. Importantly, it also enables the demonstration of tangible results that directly correlate with an employee's contributions.

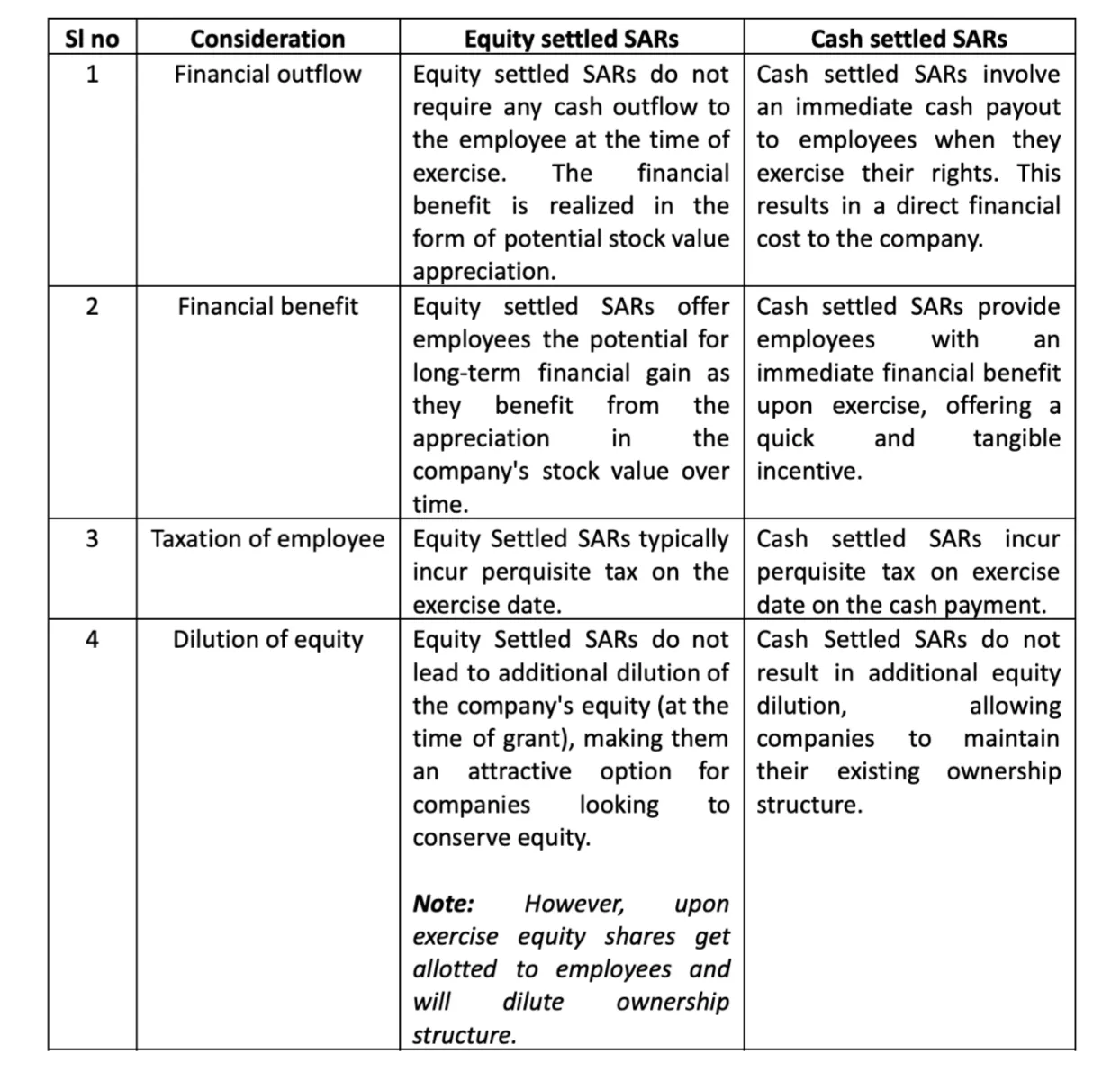

6. What is the difference between Equity Settled SAR and Cash Settled SAR?

- Equity Settled SAR: When an employee exercises their SAR, they receive the appreciation in the company's share price is settled in the form of allotment of company shares.

- Cash Settled SAR: When an employee exercises their SAR, they receive a cash payout equivalent to the appreciation in the company's share price.

To gain a thorough understanding of the implementation and settlement of SAR (Stock Appreciation Rights), we can delve into a detailed illustration.

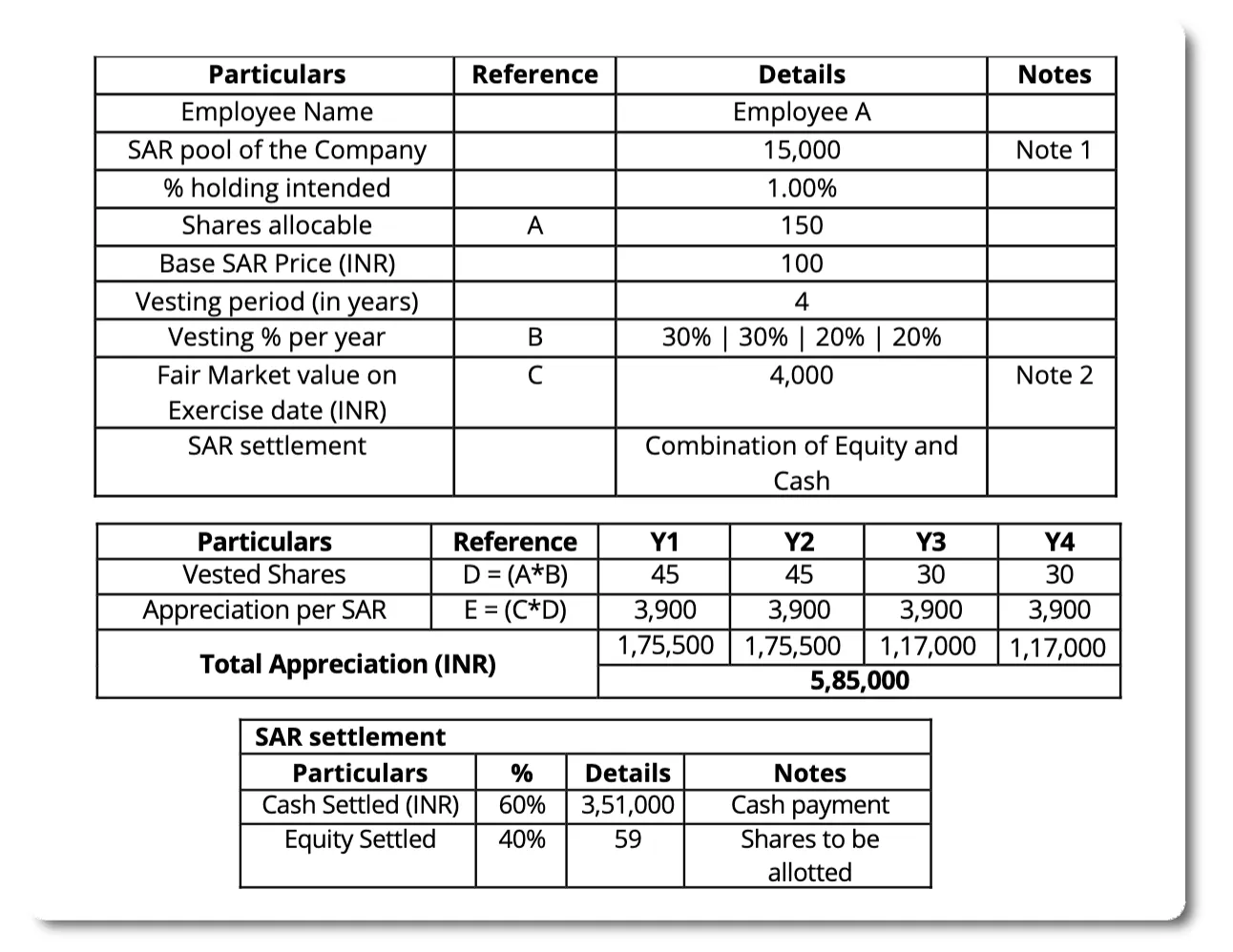

Illustration: A Company grants 1% of the SAR pool to an employee today, at a base SAR price of INR 100 per SAR, with a graded vesting of 30% for the first two years and 20% for the balance years. SAR settlement in cash for the first two years and the balance will be settled in Equity shares. How would this work?

Notes:

1. ESOPs (not granted) may be converted to SARs based on approvals as per the prevalent shareholder's agreement and subject to Companies Act, 2013. Reclassification from ESOP to SAR will reduce the ESOP pool and move to SAR pool, which will not be dilutive to other shareholders.

2. The fair market value shall be determined based on the valuation report of the company. For the illustration, assumed that the employee exercises SARs at the end of vesting period (Y4).

For startups, it may be best to retain the flexibility to decide whether SARs are settled in cash or equity, allowing the company to choose the option that best aligns with its current financial situation and strategic ownership objectives. This adaptable approach helps startups navigate capital constraints while also managing equity dilution, striking a balance that supports their long-term goals.

7. What factors should startups weigh when choosing between Equity Settled and Cash Settled SARs for their employee incentive plans?

The choice depends on factors such as ownership goals, financial benefits, employee motivation, and long-term alignment with company objectives.

8. What factors should a startup consider when designing and implementing SARs?

- Selection of employees:

- Identify which employees/level of employees within the startups should receive SARs.

- Startups can consider their roles, contributions, and significance in achieving the company's objectives.

- Timing and quantity of grants:

- Determine when SARs will be granted to eligible employees and number of SARs each employee will receive.

- Define the timing for SAR grants, deciding whether they will occur annually, quarterly, or upon the achievement of specific company milestones.

- Tailored vesting conditions:

- Customise vesting conditions to align with the startup's goals and consider employee feedback to match desired compensation outcomes.

- Evaluate whether time-based vesting, performance-based vesting, or a combination will provide the strongest incentive for employees in the Indian business environment.

- Special vesting rules: Establish special vesting rules for exceptional circumstances, such as death, disability, or other events. Determine how SARs will be managed in these situations.

- Communication plan: Educate eligible employees about the SAR program, including its benefits, terms, and how it aligns with the startup's objectives.

- Legal and regulatory compliance: From a startup's perspective when designing and implementing SARs, it is important to acknowledge the absence of specific SAR regulations, typically aligning them with ESOP guidelines under the Companies Act, 2013 and Companies Rules, 2014, and considering SEBI's SBEB regulations for best practice alignment.

- Expert consultation: Seek guidance from legal, financial, and tax experts to ensure that the SAR plan is well-structured and compliant with Indian laws and regulations.

- Employee feedback: Consider gathering feedback from the employees to understand their preferences and concerns regarding the SAR program. This feedback can assist in refining the plan to better align with the employee's expectations.

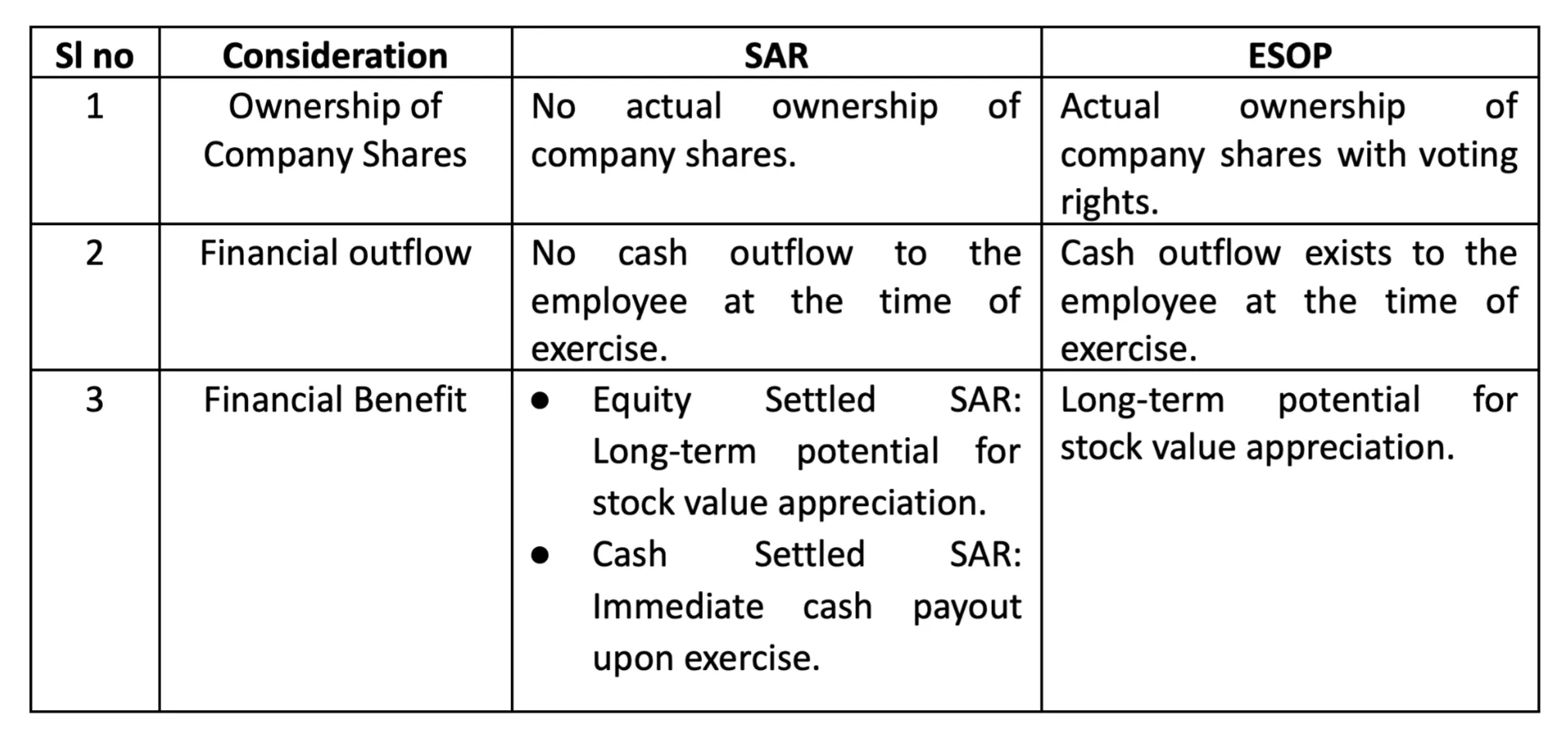

9. What are the key differences between SARs and ESOPs?

The key differences are as follows:

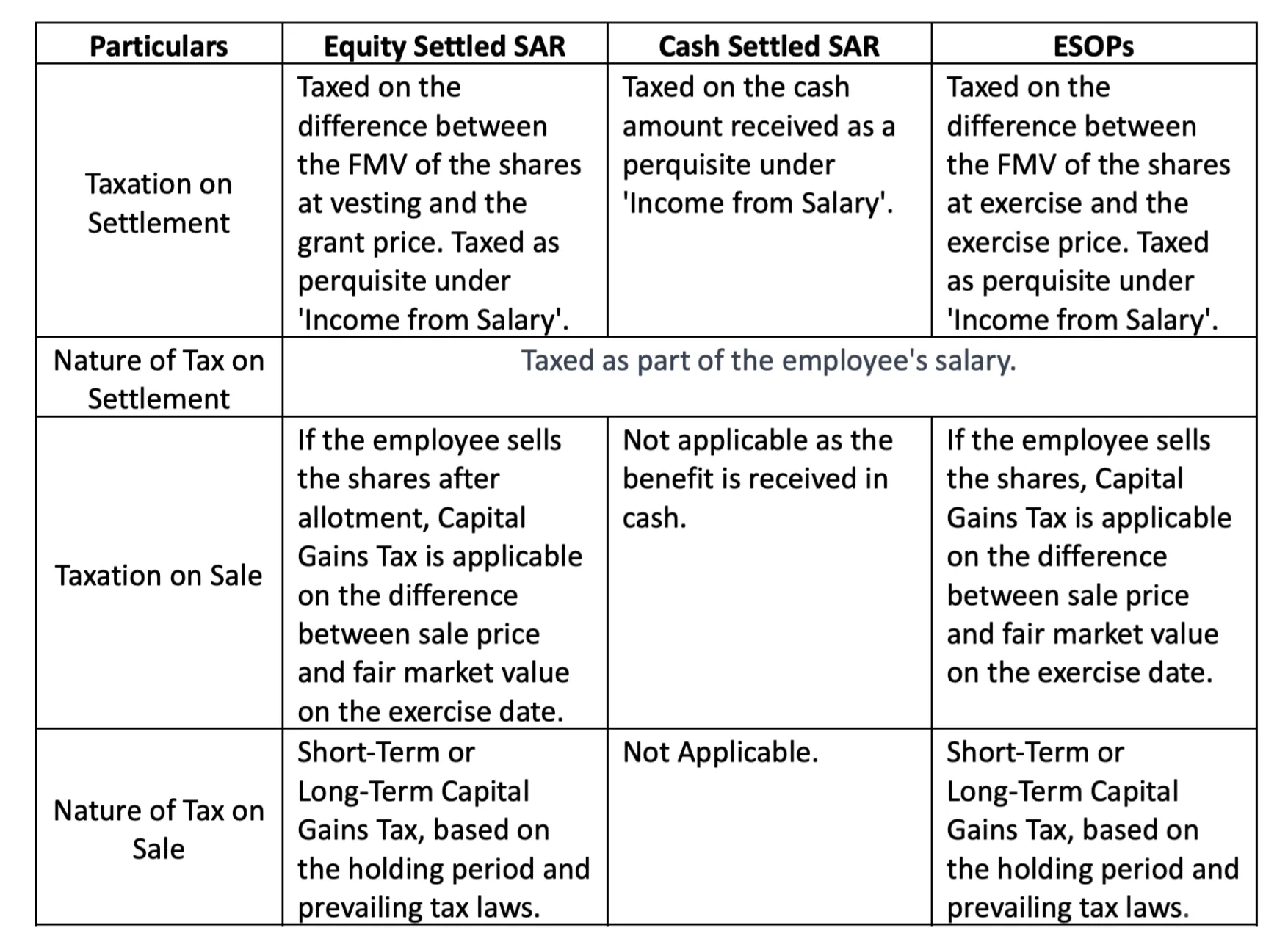

10. How do the tax implications differ for employees between Stock Appreciation Rights (SARs) and Employee Stock Option Plans (ESOPs)?

11. What are the regulations or rules governing issue of SARs by startups in India?

- While there are no specific regulations governing Stock Appreciation Rights (SARs) for startups, since the Companies Act, 2013, and the related Companies Rules, 2014 govern the issuance of shares and ESOP, as good governance and pre-empting any regulatory compliance, companies have generally followed regulations and procedures applicable to ESOP adoption.

- For implementing SARs, unlisted companies often treat them as a variation of Employee Stock Option Plans (ESOPs) and follow the procedural requirements for ESOPs outlined in relevant company rules. Additionally, they may refer to SEBI (Securities and Exchange Board of India) SBEB (Share-Based Employee Benefits) regulations as a best practice, adapting them to their specific needs where applicable.

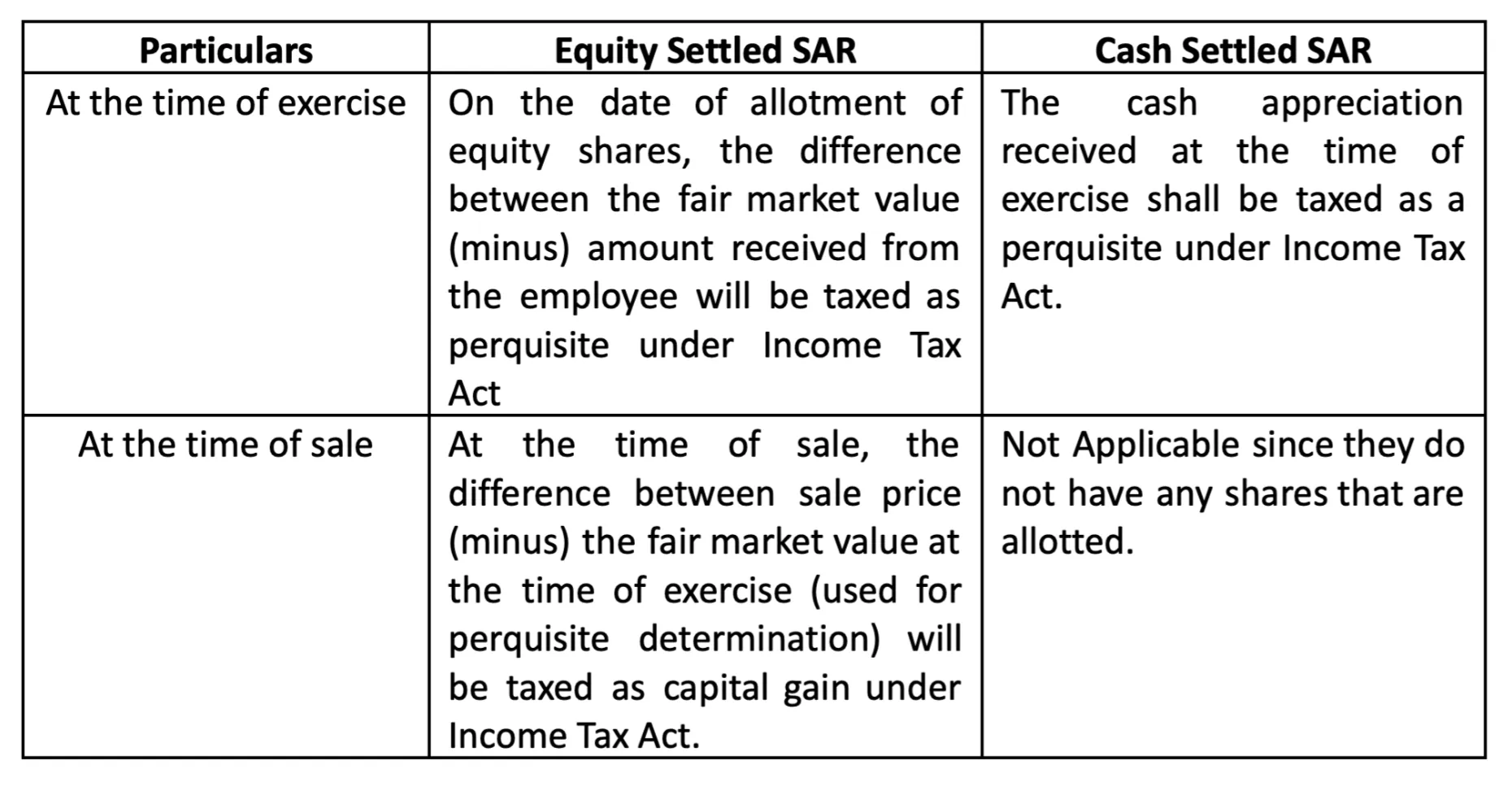

12. What are the tax implications for employees in relation to SAR?

The tax implications in the hands of the employees are as follows:

13. What key trends are emerging in employee incentive plans for unlisted companies?

a) Increased adoption of annual grants: A rising trend among unlisted companies is the preference for annual grants over other methods. This shift towards annual grants, increasing from 72% in FY19 to 80% in FY23, indicates a move towards more structured and regular incentivisation practices.

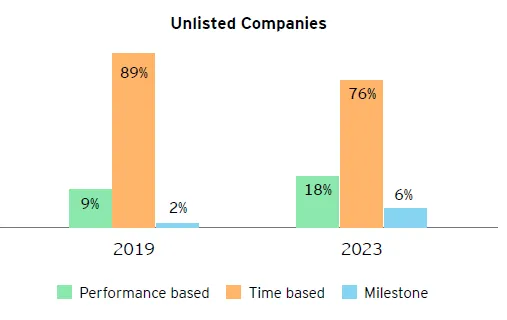

b) Movement towards performance and milestone-based vesting: There is a declining trend in the adoption of time-based vesting, which fell from 89% in FY19 to 76% in FY23. Simultaneously, there is an increasing preference for performance and milestone-based vesting, with performance-based vesting nearly doubling and milestone-based vesting more than doubling within the same period. This trend suggests a greater emphasis on aligning employee rewards with specific achievements and overall company performance.

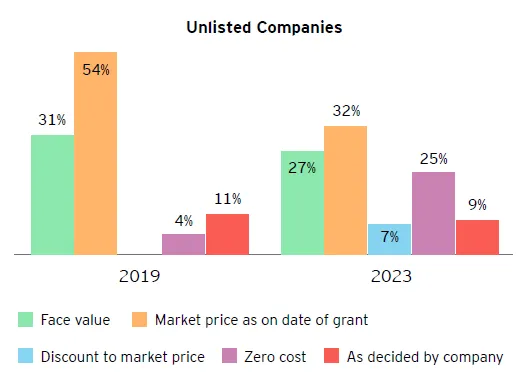

c) Shift Towards Cost-Efficiency: The trend is moving away from traditional approaches that rely on face value and market price at the time of the grant. In 2019, 54% of companies used this method, but by 2023, it dropped to 32%. Meanwhile, there is a noticeable surge in preferences for zero-cost options, which jumped from 4% to 27%, and for valuations decided by the company, which rose from 11% to 25%. This emerging trend underscores a move towards cost-effective strategies and greater corporate discretion in determining the value of incentive plans.

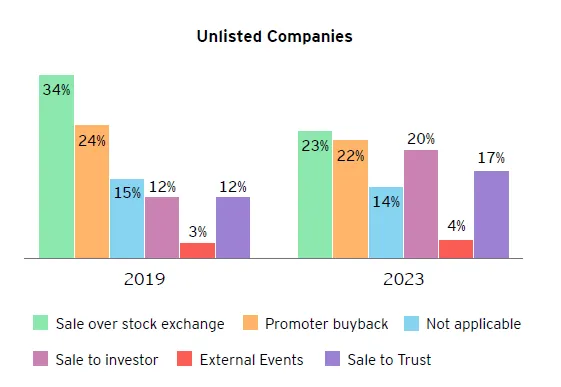

d) Positive shifts in exit strategies: The emerging exit strategy trend for unlisted companies between 2019 and 2023 reveals a positive shift towards more private and strategic liquidity options. Sales to trusts have shown a significant increase from 3% to 14%, indicating a move towards structured exits that offer beneficial scenarios for employees. Meanwhile, the approach of sale to investors, despite a decrease from 34% to 23%, still represents a substantial portion of exit strategies, underscoring its ongoing importance. This suggests a balanced and flexible exit environment, where employees have the potential to realize their incentives through a variety of channels.

In the rapidly changing landscape of corporate India, innovative employee incentives like Stock Appreciation Rights (SARs) mark a significant strategic transformation. Amid the flourishing startup scene and intense talent rivalry, SARs stand out as a dynamic and effective means to harmonize employee and corporate objectives. This shift indicates a deeper understanding of what motivates employees and the importance of cultivating long-term value.

As we look to the future, it is apparent that innovative employee incentive programs will be key in shaping corporate cultures and enhancing employee engagement. SARs, versatile in navigating economic changes, are vital in not only attracting and retaining top talent but also fostering a culture of mutual growth and success.

Companies that adopt innovative approaches are poised to flourish in India's evolving business ecosystem, establishing a mutually beneficial relationship between organisational goals and employee welfare.

DISCLAIMER

The views expressed herein are those of the author as of the publication date and are subject to change without notice. Neither the author nor any of the entities under the 3one4 Capital Group have any obligation to update the content. This publications are for informational and educational purposes only and should not be construed as providing any advisory service (including financial, regulatory, or legal). It does not constitute an offer to sell or a solicitation to buy any securities or related financial instruments in any jurisdiction. Readers should perform their own due diligence and consult with relevant advisors before taking any decisions. Any reliance on the information herein is at the reader's own risk, and 3one4 Capital Group assumes no liability for any such reliance.Certain information is based on third-party sources believed to be reliable, but neither the author nor 3one4 Capital Group guarantees its accuracy, recency or completeness. There has been no independent verification of such information or the assumptions on which such information is based, unless expressly mentioned otherwise. References to specific companies, securities, or investment strategies are not endorsements. Unauthorized reproduction, distribution, or use of this document, in whole or in part, is prohibited without prior written consent from the author and/or the 3one4 Capital Group.