The Economics Behind: The True Cost of Debt for Startups

If you have followed Parts I (A Startup’s Optimum Capital Structure) and II (Integrating Debt into the Capital Mix) of this startup debt series, you are already familiar with the more appealing aspects of raising debt capital. In Part I, we examined the optimisation of a startup's capital structure and how debt can effectively reduce the blended cost of capital. In Part II, we explored various scenarios in which debt can serve as a valuable tool for startups, allowing them to conserve equity capital and extend their operational runway.

At this point, you may be questioning the necessity of Part III. What additional insights could there possibly be regarding debt financing?

This article addresses those inquiries by focusing on the critical yet often overlooked aspects of assessing your ability to repay debt and evaluating the key factors when considering your debt options. Financial and non-financial covenants, runway stress testing, and the implications of founder personal guarantees may not be the most glamorous topics, but they are essential considerations that should not be disregarded.

In this article, we will delve into these less discussed aspects of raising debt, the potential consequences of securing financing without a thorough evaluation of repayability and covenant compliance, and provide insight into how 3one4 approaches debt assessment and viability during the early stages of a company's lifecycle.

Ascertaining your Ability to Repay Debt

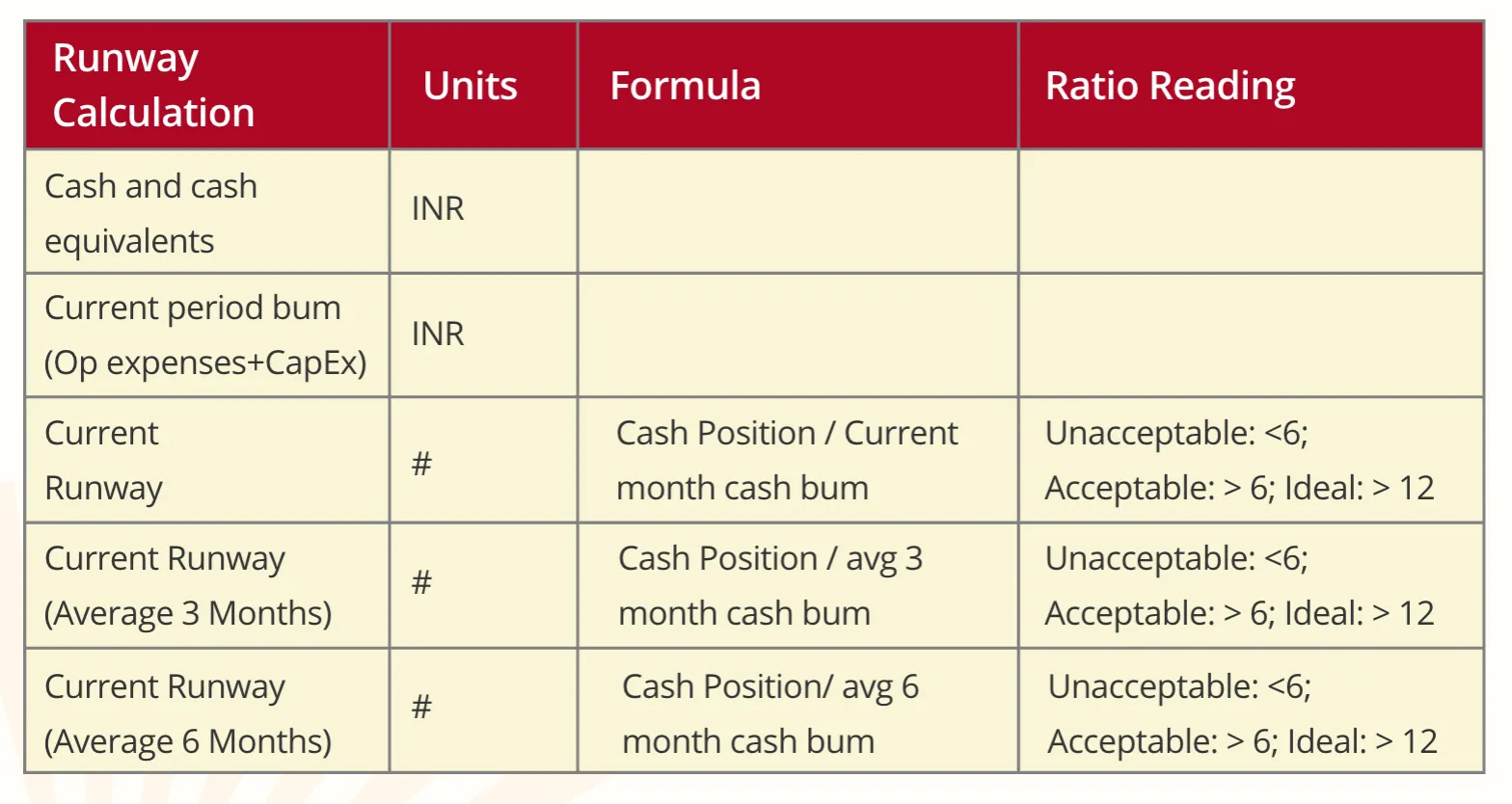

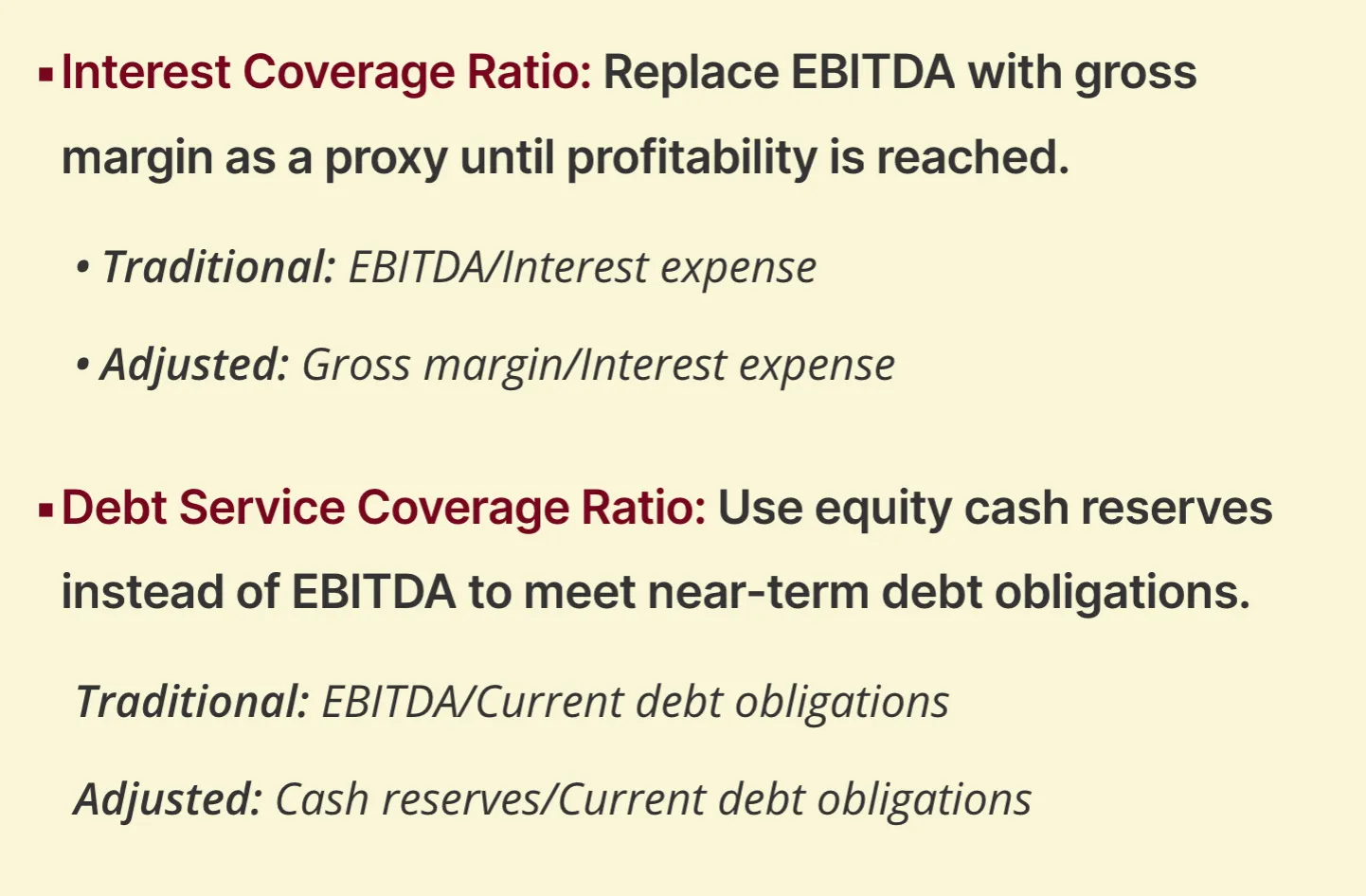

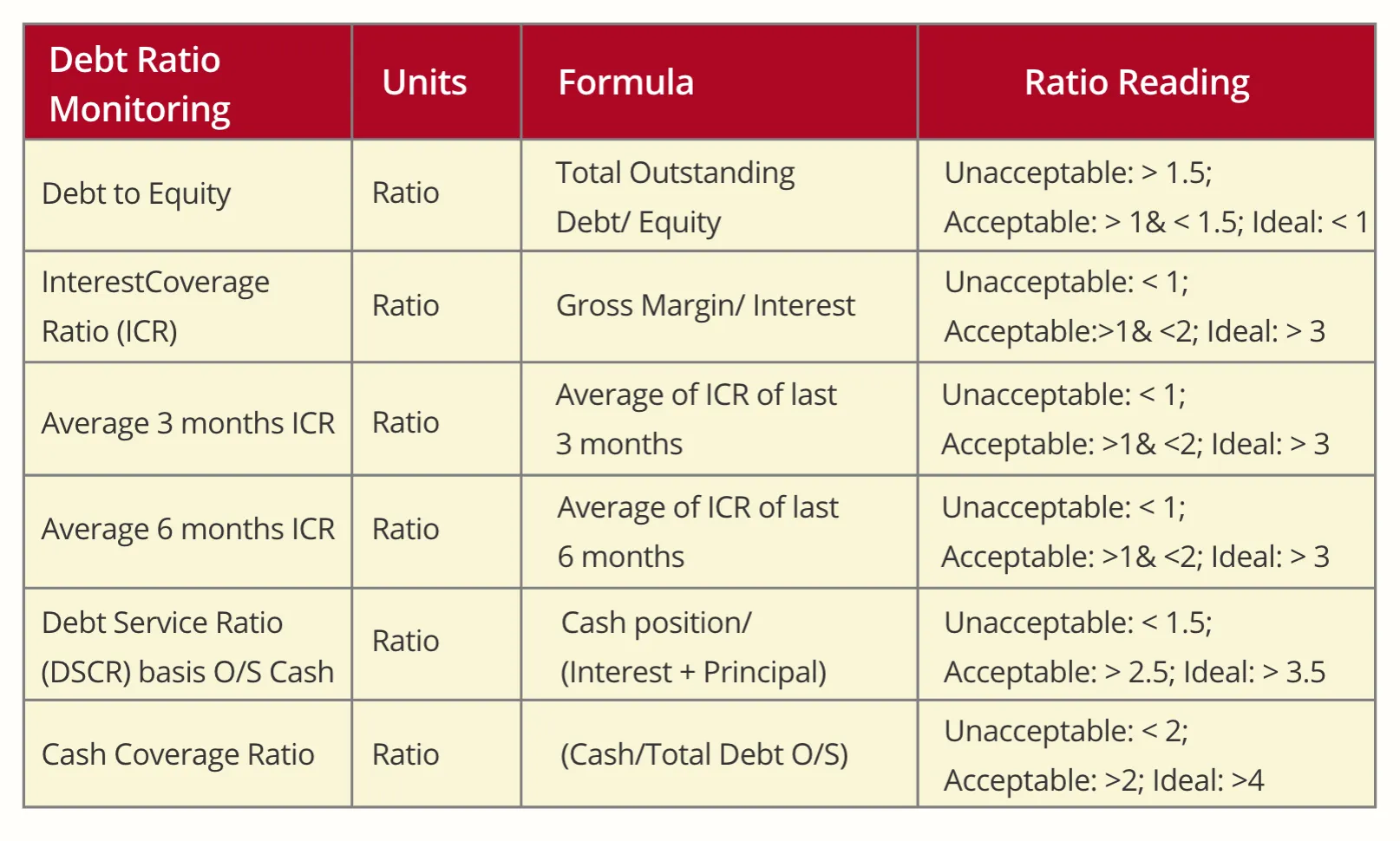

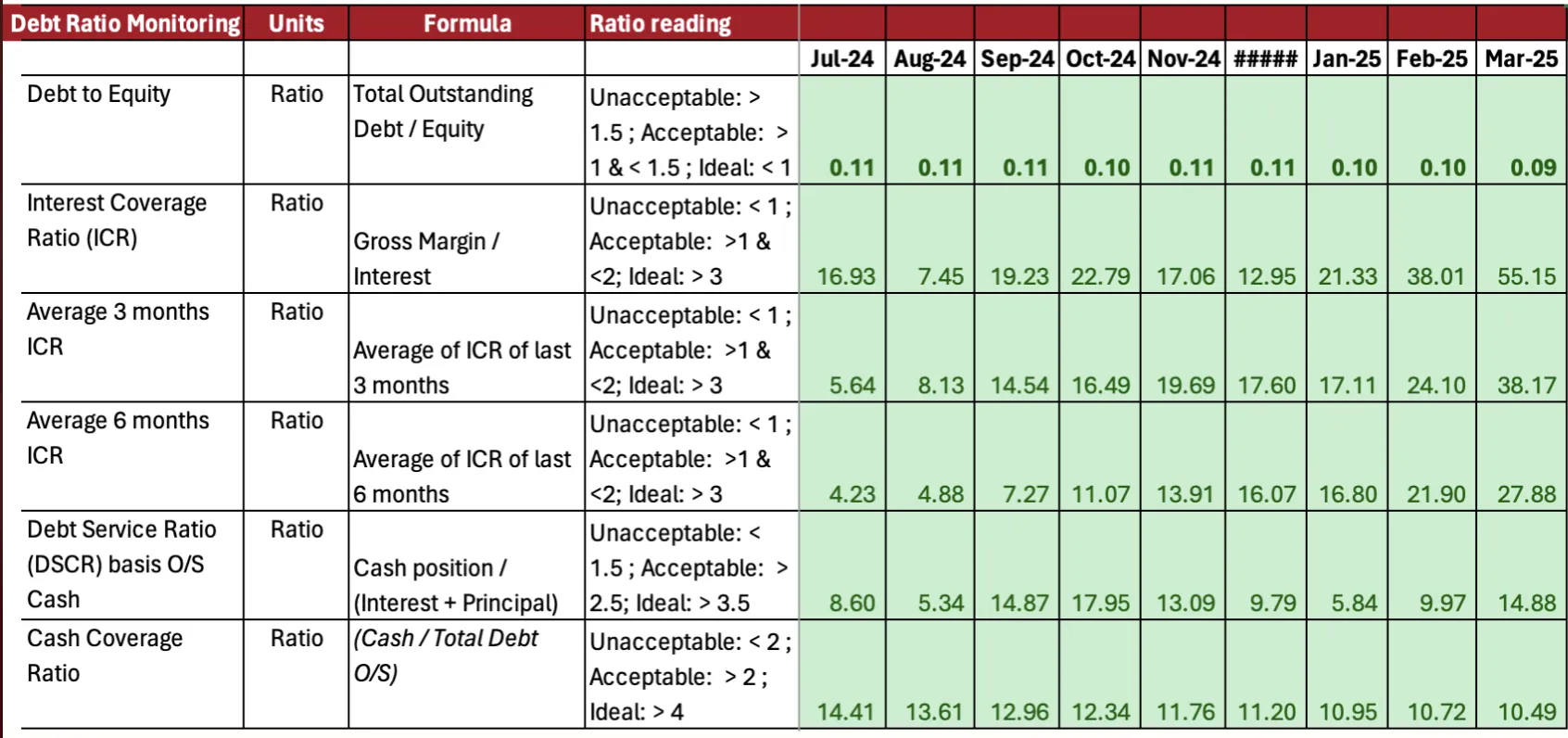

Traditionally, debt repayment is sourced from the profits a company generates through its business operations. Standard profitability ratios, such as the Interest Coverage Ratio (ICR) and Debt Service Coverage Ratio (DSCR), are utilized to assess a company’s financial health with respect to its debt obligations. These ratios are based on the assumption that the company generates profits well in excess of the minimum required to meet principal and interest repayment obligations.

However, within the lifecycle of a startup, profitability is often achieved at a later stage. Startups, particularly in their pursuit of rapid growth, are generally expected to incur losses rather than generate profits during their early phases. Consequently, startups cannot be assessed through the same financial metrics as established, profit-generating corporations when evaluating their debt position.

Runway Ascertainment & Stress Testing

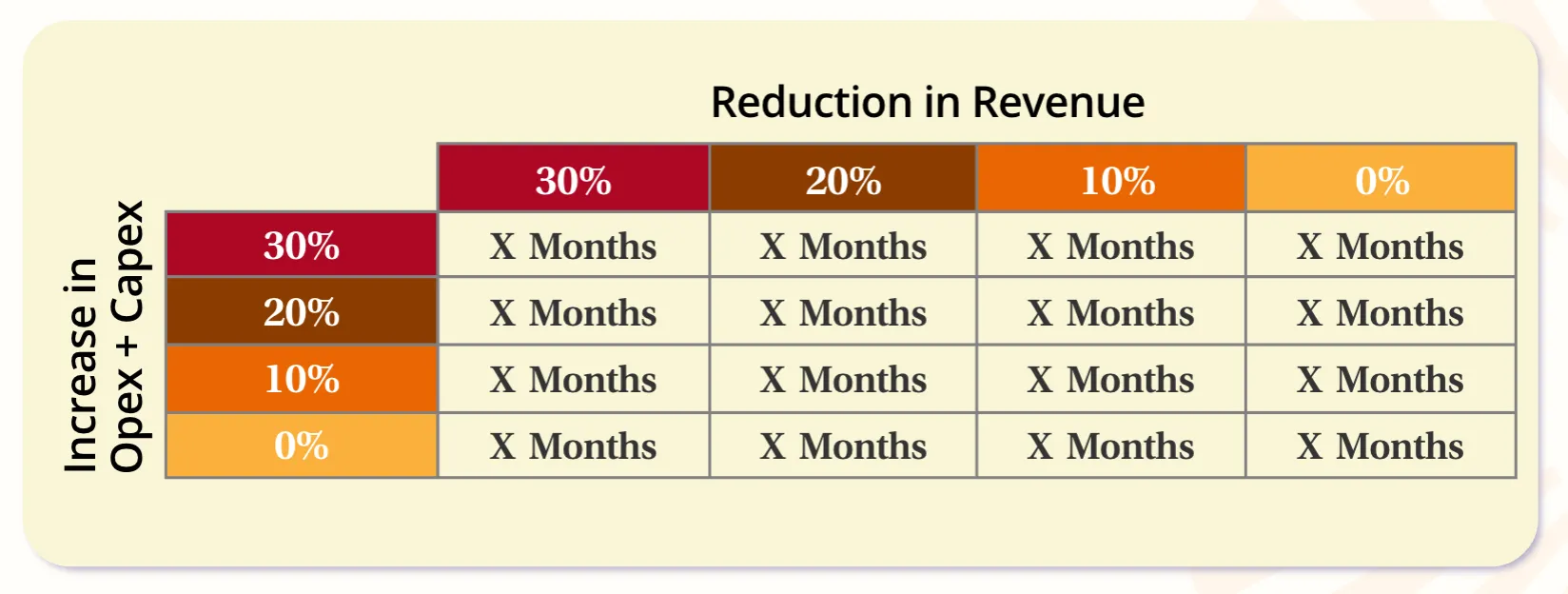

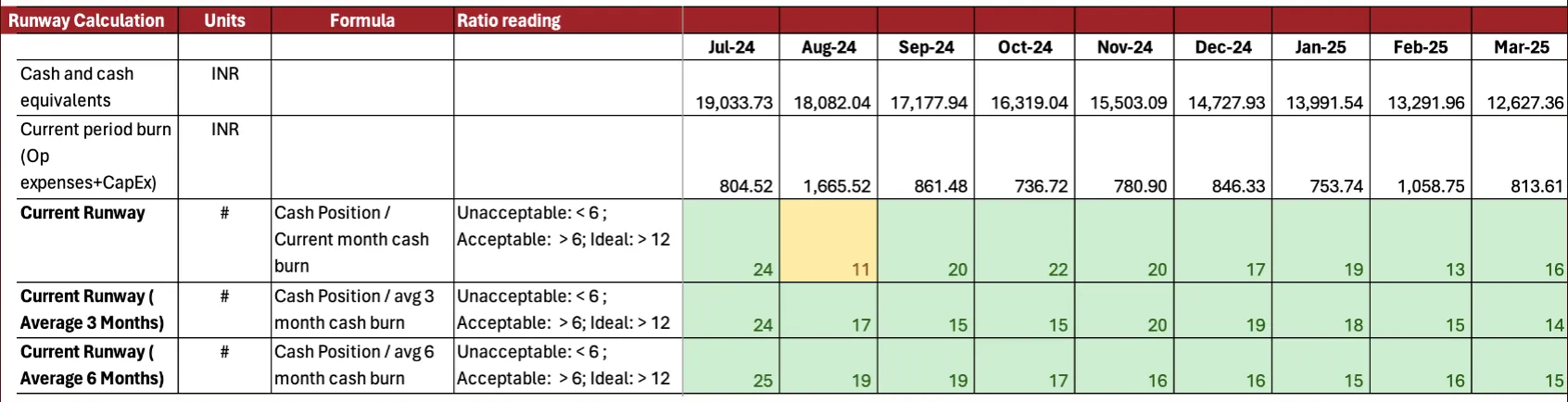

The runway, defined as the capacity of available cash to sustain business operations, is a critical indicator of a startup’s viability. It plays a central role in guiding management’s decisions regarding capital raises and capital allocation.

It is imperative for a startup to assess its runway both before and after taking on any debt. By accounting for the fixed obligations associated with principal and interest repayments, the startup must ensure that it has sufficient runway to achieve its financial and operational milestones, which serve as benchmarks for securing subsequent funding rounds.

In addition to calculating its projected runway, a startup must also account for the inherent uncertainty of its cash inflows and outflows. This necessitates conducting a series of stress tests designed to simulate the impact of force majeure events. These Runway Stress Tests provide management with insights on controlling future cash burn and help estimate the startup’s runway under unforeseen circumstances.

At 3one4, prior to approving any debt transaction with a portfolio company, we conduct an internal runway stress test, as well as, analysis based on the following criteria:

Reducing Cash Conversion Cycle

The Cash Conversion Cycle (CCC) is a financial metric that measures the time it takes for a company to convert its investments in inventory and other resources into cash inflows from sales. It reflects the number of days between the payment for raw materials or inventory and the receipt of cash from the sale of the final product or service.

A shorter CCC indicates efficient management of inventory, accounts receivable, and accounts payable, while a longer cycle suggests the opposite.

This metric is relevant to any startup that has commenced monetisation, not only those involved in the manufacturing of physical products. The CCC is typically elevated in the early stages of a startup's lifecycle.

To calculate a startup's cash conversion cycle, the following formula can be applied:

.webp)

In essence, the longer the cash conversion cycle, the greater the requirement for debt capital. A thorough understanding and optimization of this metric, to the extent possible, can lead to reduced debt obligations.

Retooling the Existing Profitability Ratios

Given the lack of profitability in startups, a modification of traditional ratios is necessary to accurately estimate the amount of debt a startup can secure and its ability to meet debt obligations.

Instead of relying on the common metric of positive EBITDA, alternative measures such as equity cash reserves and gross margins can be employed, depending on the ratio:

In addition to conducting a runway analysis, at 3one4, we also evaluate the following adjusted ratios before approving any debt transactions:

Key Aspects to Factor in Debt Assessment

After a company has identified its use case for debt, assessed its debt requirements, and evaluated its ability to repay, one might wonder, "What else is there to do?"

There is, however, one crucial step remaining before finalizing the process and expecting the debt funds to be disbursed: analyzing the sanction letter and its various hidden terms.

A sanction letter can be complex and, for some, difficult to navigate. The legal terminology, references to LIBOR, MCLR, and conditions that may trigger additional interest charges, can seem daunting, as they should, given their potential impact on the company.

It is essential to carefully review the key aspects of the sanction letter before signing it, and we will now discuss those important considerations.

True cost of Capital

What is the true cost of capital for the debt you are seeking to secure?

Most term sheets begin with the "Total Sanction Amount and the Interest Rate (%)", and this is often where companies stop scrutinizing. After navigating numerous challenges to finally receive the sanction letter, the relief of seeing the final sanction amount may lead to a hasty decision to sign.

While the interest rate mentioned in the term sheet is indeed an important factor, the question remains: what is the true cost of that interest?

The actual interest a company ends up paying to the lender can only be accurately assessed by calculating the Internal Rate of Return (IRR) on all costs associated with the debt. These costs typically include:

- Processing fees required at the time of securing the loan

- Moratorium on principal/interest provided by the lender

- Cash margin/collateral to be held by the lender or as a fixed deposit with a charge to the lender

- Loan repayment tenure

- Other upfront expenses

To understand the difference between the interest rate mentioned in a sanction letter and the final true cost of capital, consider the following example:

Company X has received a sanction letter from MMMP Bank for a term loan to address its asset-liability mismatch (refer to Part II of the debt series for more on ALM mismatch), which has affected its financial position. The sanction letter includes the following key terms:

- Loan Principal Amount: INR 10 crore

- Interest Rate: 13.50% per annum

- Tenure: 3 years (36 months) from 31st July 2024

- Non-refundable processing fee: 1% of the loan principal (payable upfront)

- Moratorium on principal: 6 months from the issue of the loan (31st January 2025)

- Cash margin (Fixed Deposit lien with MMMP Bank): INR 2.5 crore

- Due diligence, transaction documentation, and other expenses: INR 5 lakhs

- Penal interest on default: 2% per month

- Prepayment charges: 2% of the outstanding principal loan

- Minimum runway requirement: 6 months

- Minimum Debt-to-Equity ratio: 1x

While a 13.50% interest rate might initially seem favourable, what would the true cost of capital look like when all associated costs are factored in?

Understanding the full scope of costs is critical to making an informed decision.

At 3one4, prior to closure of any debt transaction, we perform the analysis of the True cost of capital in this framework for Company X:

.png)

- The processing fees and additional expenses have imposed a financial burden on the company amounting to INR 16.8 lakhs.

- The cash margin requirement has led to an outflow of INR 2.5 crore in July 2024, resulting in an opportunity cost for the entire loan tenure [subsidised by an Interest on the cash margin at 7% p.a.), as these funds will only be returned in July 2027.

- For this analysis, we have assumed that Company X does not default on any loan instalments and does not opt for early loan prepayment. Both of these scenarios would lead to an even higher XIRR (%) than depicted.

As illustrated, the interest rate of 13.5% per annum translates into an XIRR of 21.2% after accounting for all associated costs, which represents the true cost of capital for Company X.

Debt Covenants

In addition to carefully reviewing the fine print of a term sheet, Company X must also take into account the financial debt covenants it is required to maintain throughout the loan tenure. It is crucial to fully understand these covenants and how to calculate the underlying ratios to ensure compliance, as breaching these covenants could have serious repercussions on the company’s financial health.

Runway

As part of the lender's underwriting process, the runway for Company X would have been assessed to ensure the company has sufficient cash and cash equivalents to meet its debt obligations. At early stages, this covenant typically requires maintaining a runway of 6 to 12 months.

Company X, after evaluating its runway position (based on the methodology outlined earlier in this article), has the following financial status on a current-month, 3-month, and 6-month basis:

It is important to note that Company X has taken a forward-looking approach to assess the impact on its runway.

As illustrated, the company only falls below the 12-month runway requirement in one instance but remains in compliance with the 6-month minimum covenant.

Debt to Equity Ratio

The debt-to-equity ratio formula is straightforward ([Total Outstanding Debt/Equity]), but ensuring compliance with this ratio can be challenging. This is because the equity component (the denominator) is not static and will decrease each month if the company incurs cash losses. As a result, it is essential for the company to monitor this ratio on a monthly basis.

Typical sanction letters require a debt-to-equity ratio between >0.5x & <1.2x, depending on the company's scale and risk profile.

Company X has conducted an evaluation of its debt monitoring ratios (beyond just the debt-to-equity ratio) on a forward-looking basis to ensure compliance with its financial covenants.

Company X is well within the required debt-to-equity ratio of 1x and remains healthy across all key ratios typically used by lenders to evaluate the company’s ongoing financial position.

Reporting requirements

Lenders typically require periodic reporting of a company's historical financial statements or MIS, on a monthly, quarterly, and annual basis. Additionally, the company is expected to provide annual forecasts and projections, including updates on runway, debt-to-equity, and any other ratios the lender deems necessary.

Failure to comply with any of the above covenants could result in severe consequences, including penalties, additional interest levies, or even the recall of the entire credit facility.

Personal Guarantee

The requirement for a personal guarantee has become a significant topic of discussion in debt negotiations, though the clause itself is not new. Under this clause, founders are expected to pledge their personal assets and agree to repay the debt from personal funds if the company defaults on its obligations.

Recently, there has been resistance from many founders regarding this clause, and lenders have taken note. As a result, personal guarantees are now selectively included following a detailed underwriting evaluation of the company, rather than being applied as a blanket condition in all sanction letters.

Conclusion

The early-stage debt ecosystem is still in its formative stages. Both banks and non-banking financial companies (NBFCs) are continuously refining their underwriting methodologies to adapt and enhance their traditional models for assessing creditworthiness. This ongoing evolution creates a distinct opportunity for startups to demonstrate their financial viability by presenting innovative approaches to conventional underwriting frameworks. In collaboration with these financial institutions, startups can co-create tailored debt solutions, driving transformative change within the broader credit ecosystem.

DISCLAIMER

The views expressed herein are those of the author as of the publication date and are subject to change without notice. Neither the author nor any of the entities under the 3one4 Capital Group have any obligation to update the content. This publications are for informational and educational purposes only and should not be construed as providing any advisory service (including financial, regulatory, or legal). It does not constitute an offer to sell or a solicitation to buy any securities or related financial instruments in any jurisdiction. Readers should perform their own due diligence and consult with relevant advisors before taking any decisions. Any reliance on the information herein is at the reader's own risk, and 3one4 Capital Group assumes no liability for any such reliance. Certain information is based on third-party sources believed to be reliable, but neither the author nor 3one4 Capital Group guarantees its accuracy, recency or completeness. There has been no independent verification of such information or the assumptions on which such information is based, unless expressly mentioned otherwise. References to specific companies, securities, or investment strategies are not endorsements. Unauthorized reproduction, distribution, or use of this document, in whole or in part, is prohibited without prior written consent from the author and/or the 3one4 Capital Group.

.jpg)