India’s Wealth Management Industry

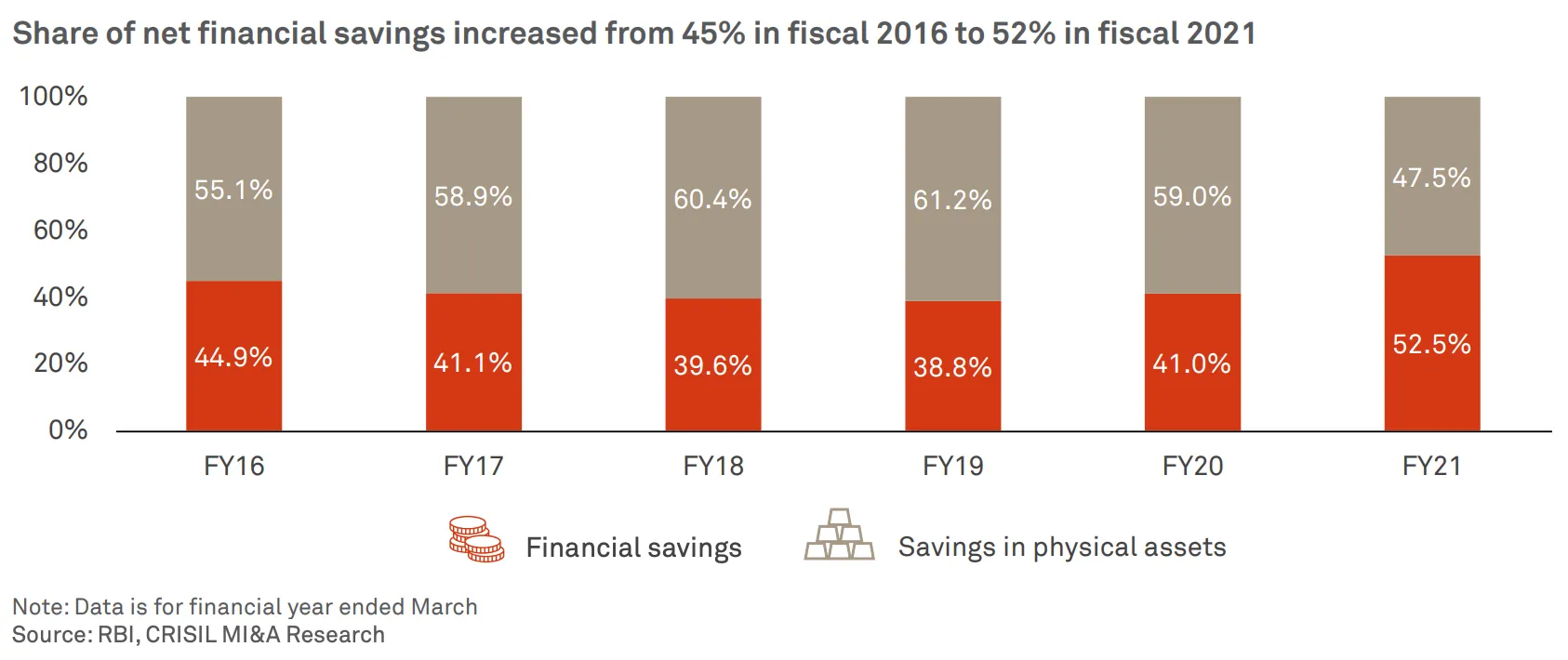

The Rise of Financialisation of Savings in India

The wealth landscape in India is undergoing a significant transformation driven by rising average income, increasing financial literacy and awareness, proliferation of digital financial services and the strong performance of Indian capital markets.

.webp)

Indian investors are exploring newer avenues to drive sustained wealth creation, resulting in a tectonic shift in the way we save and invest:

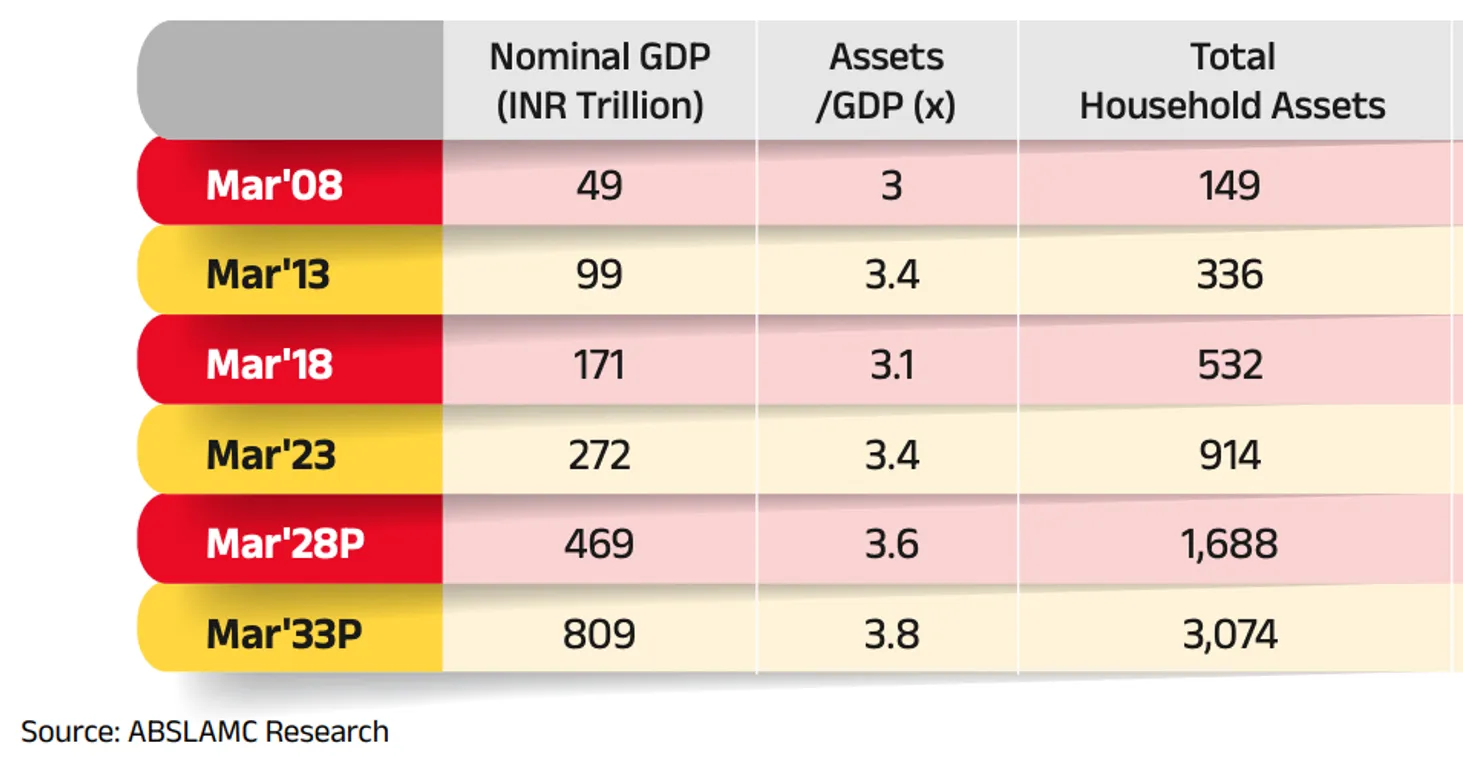

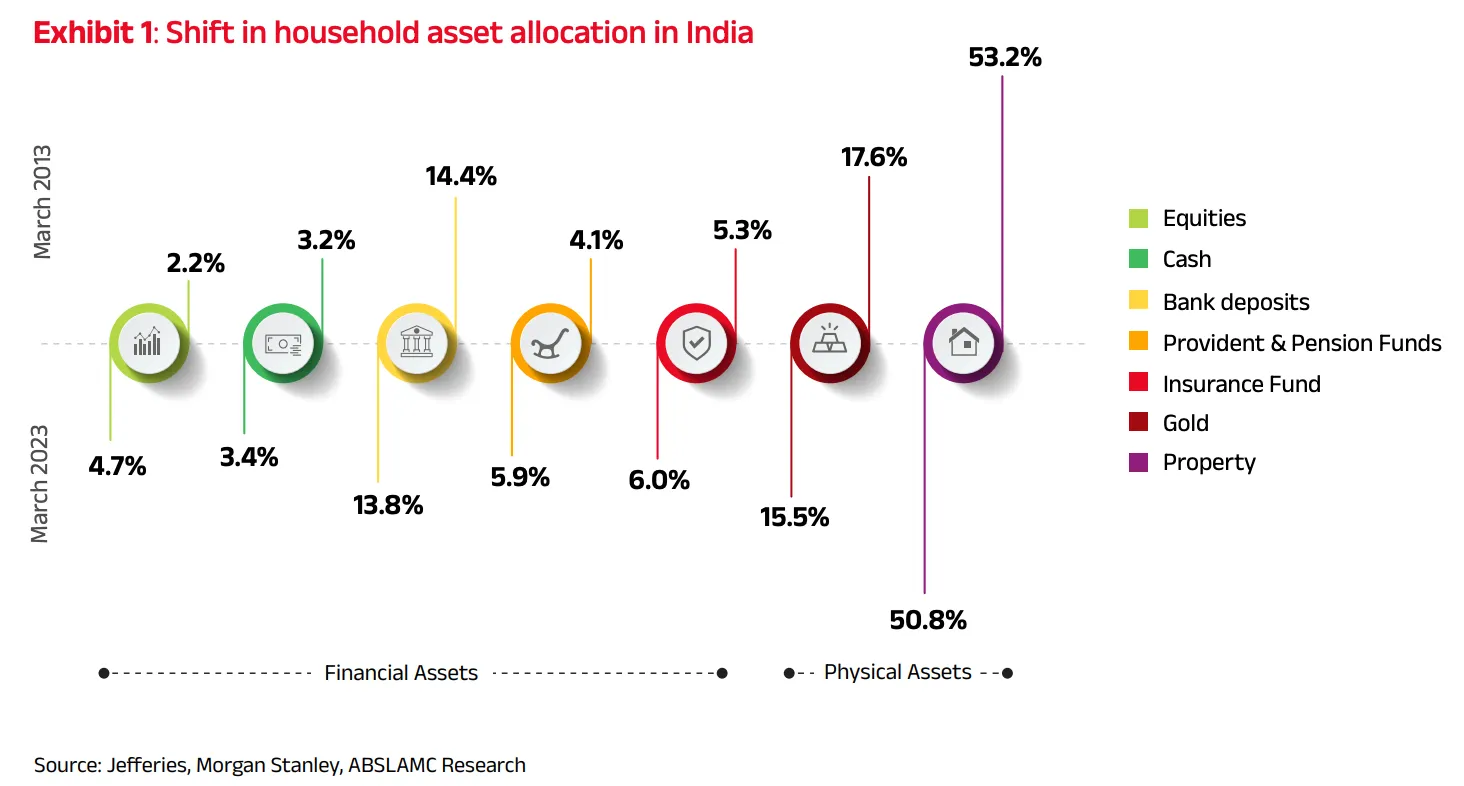

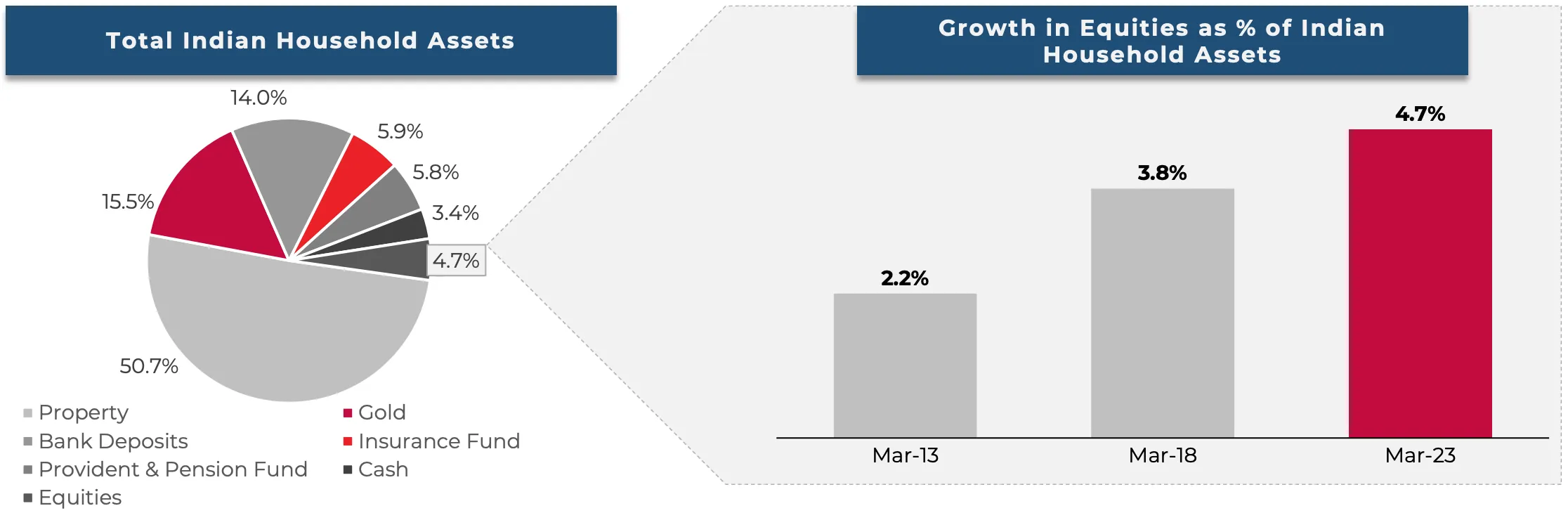

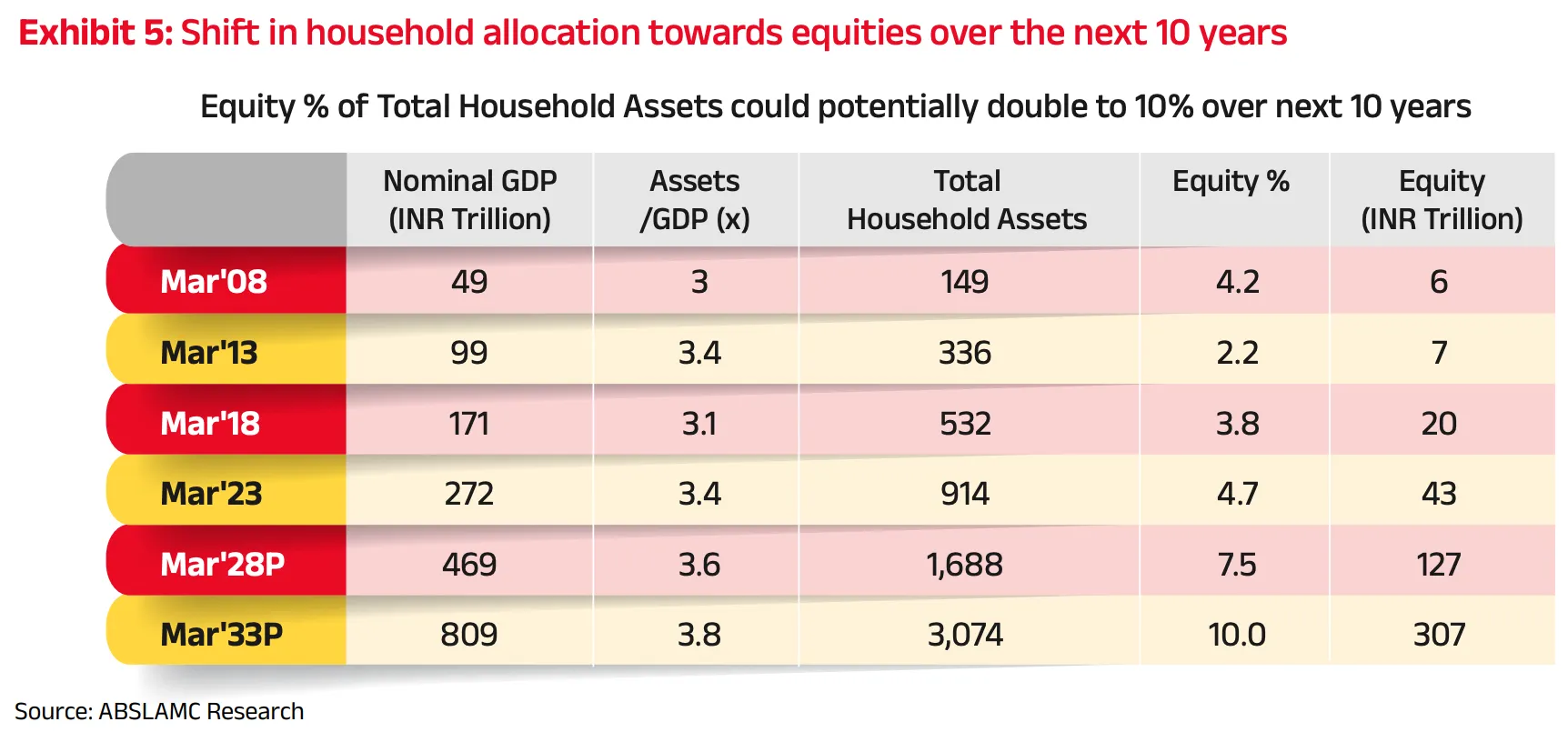

The total household assets in India have grown significantly, increasing from INR 336 trillion in 2013 to INR 914 trillion in 2023, ~3X growth over the decade.

Traditionally, Indian households have heavily favored physical assets like gold and real estate. As household incomes rise, the pursuit of more flexible and diverse investment avenues is becoming more prominent. Hence, India is witnessing a noticeable shift towards financial assets driven by changing economic dynamics and preferences.

The Iron Triangle of Wealth

The iron triangle of wealth management—returns, risk and liquidity—defines the core objectives of investors.

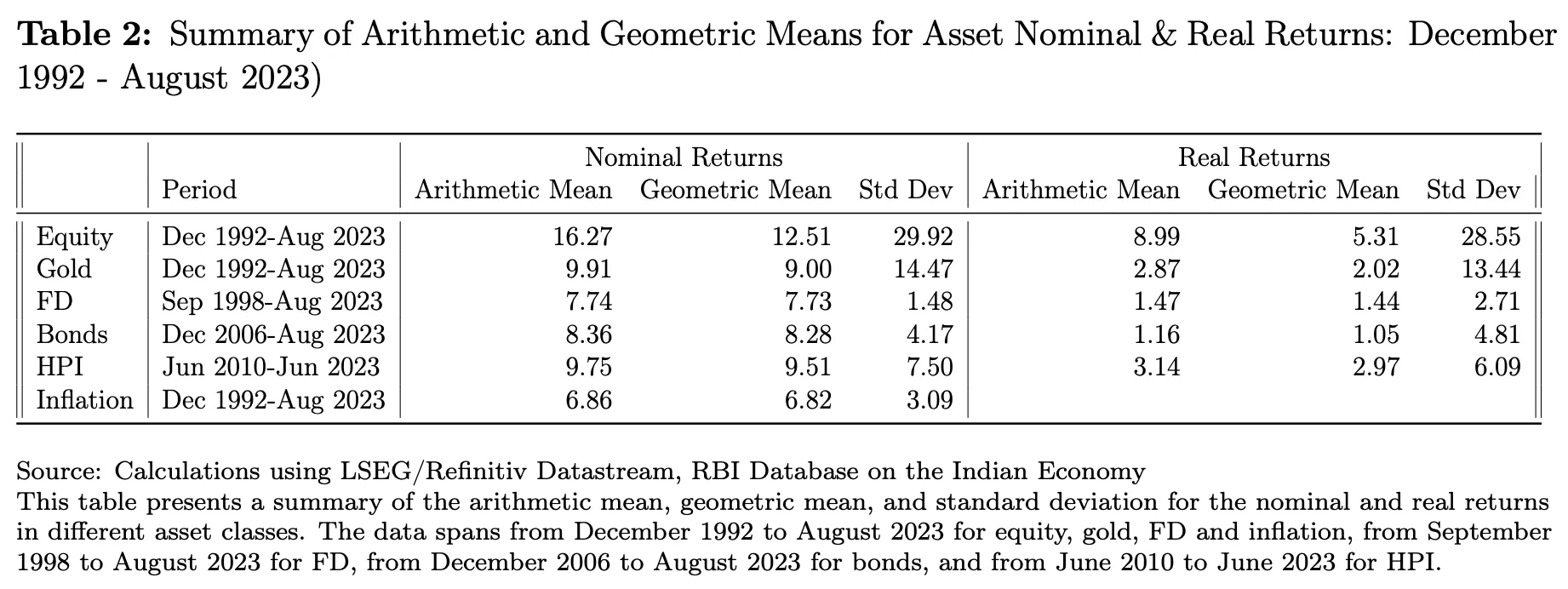

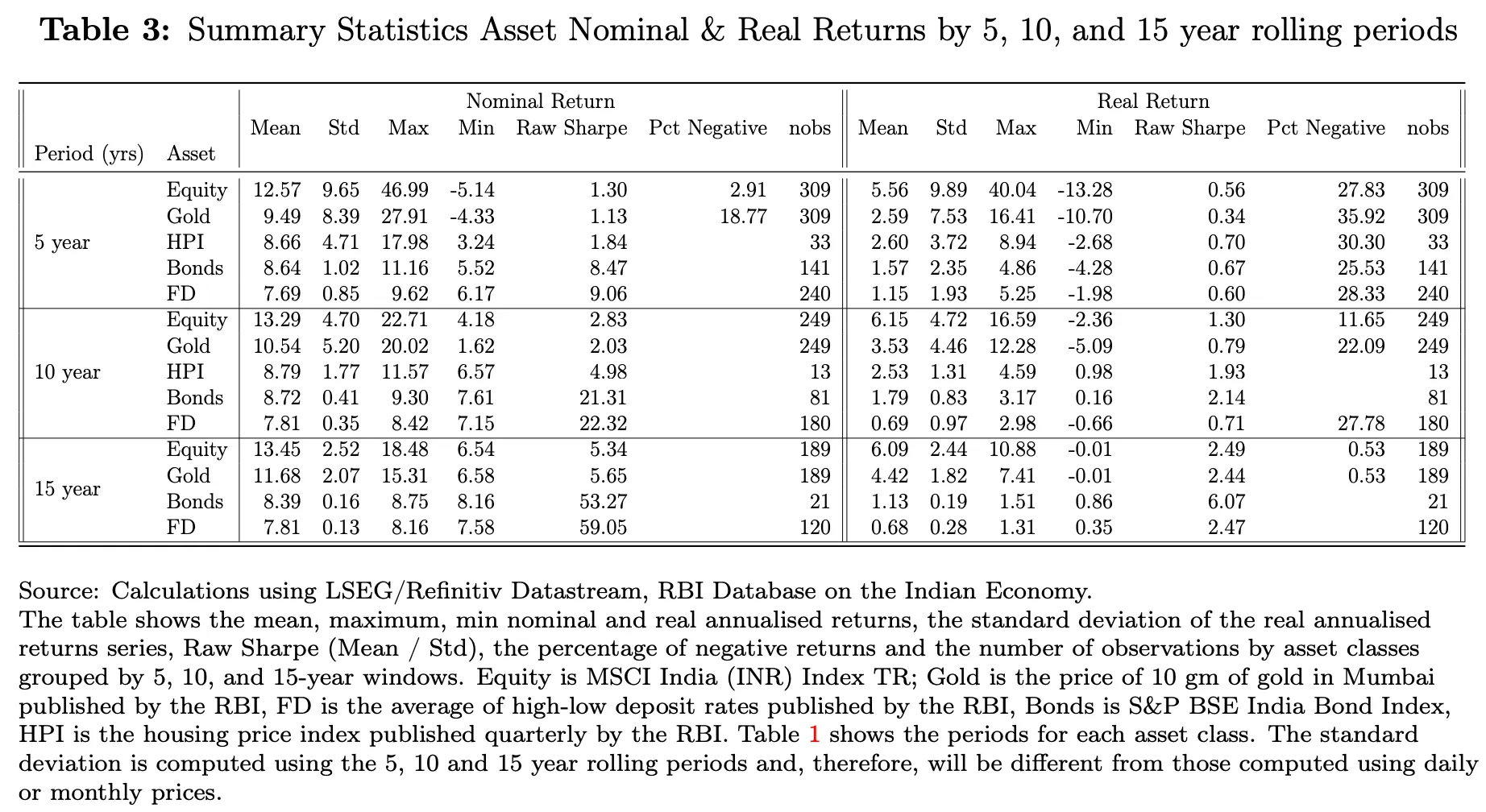

Returns: Historical analysis of return profiles of different assets reveals interesting insights highlighting the dual nature of these asset classes in the Indian market: the growth potential and risks of equities, gold’s role as an inflation hedge, the stark reality of real returns in fixed deposits, and the steady nature of bonds - driven by the role of inflation in shaping investment returns and eroding purchasing power.

It is also important to note here that on a 10 year horizon, real returns are negative for equities only 12% of the time, indicating their resilience. In 5-and-10-year rolling period, bank deposits show returns of 7.8%. On a 10 year horizon, real returns are negative 28% of the time. And cash gives negative returns on a real basis 100% of the time.

Risk

- Indian investors exhibit a diverse range of risk profiles, influenced by a multitude of factors including age, number of dependents, family background, profession, knowledge of the market, and contingency plans. Younger investors, for example, may have a higher risk tolerance, driven by their longer investment horizon and fewer financial responsibilities. In contrast, older investors or those with multiple dependents may prioritize capital preservation and stability.

- Additionally, the level of market knowledge significantly affects investment behavior. Investors well-versed in market intricacies and financial instruments tend to explore diversified portfolios, including equities, mutual funds, and alternative assets. On the other hand, those with limited market knowledge might stick to traditional investments such as fixed deposits and gold.

- While there is a widespread preference for safety and stability among Indian investors, there is also a strong desire for growth and capital appreciation. This duality leads to a blend of conservative and aggressive investment strategies. Many investors seek a balanced approach, allocating a portion of their portfolio to low-risk assets to ensure security, while simultaneously investing in higher-risk assets to achieve potential higher returns.

Liquidity

- Indian investors prioritise liquidity in their asset allocation decisions to ensure quick access to funds for emergencies or short-term goals. Highly liquid assets, such as savings accounts, fixed deposits, and certain mutual funds, are favored for their ease of conversion into cash without significantly impacting market value, providing security and stability.

- To manage risk and capitalize on growth opportunities, Indian investors adopt a balanced approach by allocating a portion of their portfolio to highly liquid assets while investing in less liquid, higher-return assets like real estate and alternative investments for long-term wealth creation. The rise of digital platforms and increasing financial literacy further support informed decision-making, optimizing asset allocation for liquidity, stability, and growth.

So really any product that’s being designed will need to strike the right balance between these three variables by choosing the right underlying assets to solve for the needs of a specific investor persona.Changing Investor DynamicsWealth management in India is at a nascent stage and presents a huge opportunity for financial services companies to cater to this emerging market with evolving investor dynamics.India's growth story is being propelled by three major megatrends: global offshoring, leadership in digitalisation, and energy transition. These trends are supported by several enablers, including sector-specific pro-growth policies, a business-friendly environment with low associated costs, increasing financialisation of savings, and rapid privatisation and asset sales. Together, these factors are driving the country's growth ambitions forward.This change in larger economic macros is also lending to changing investor dynamics:

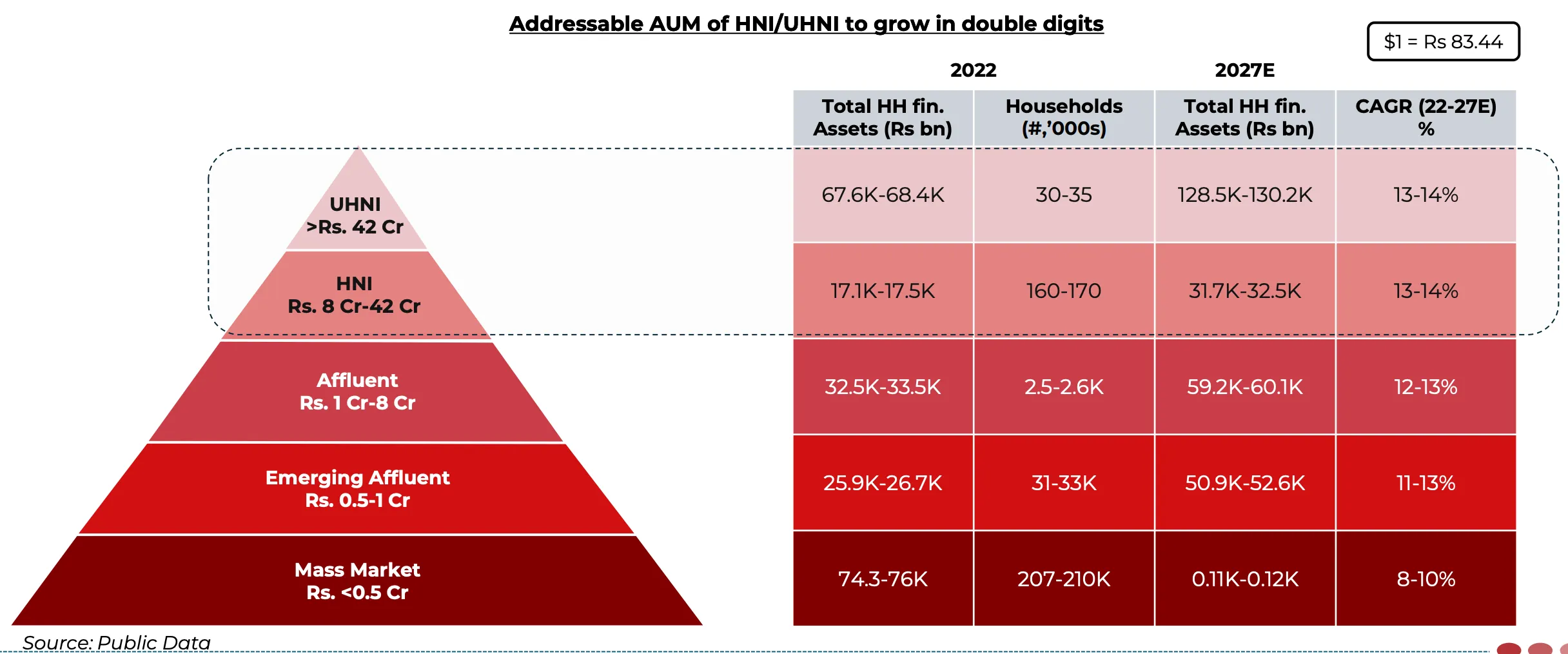

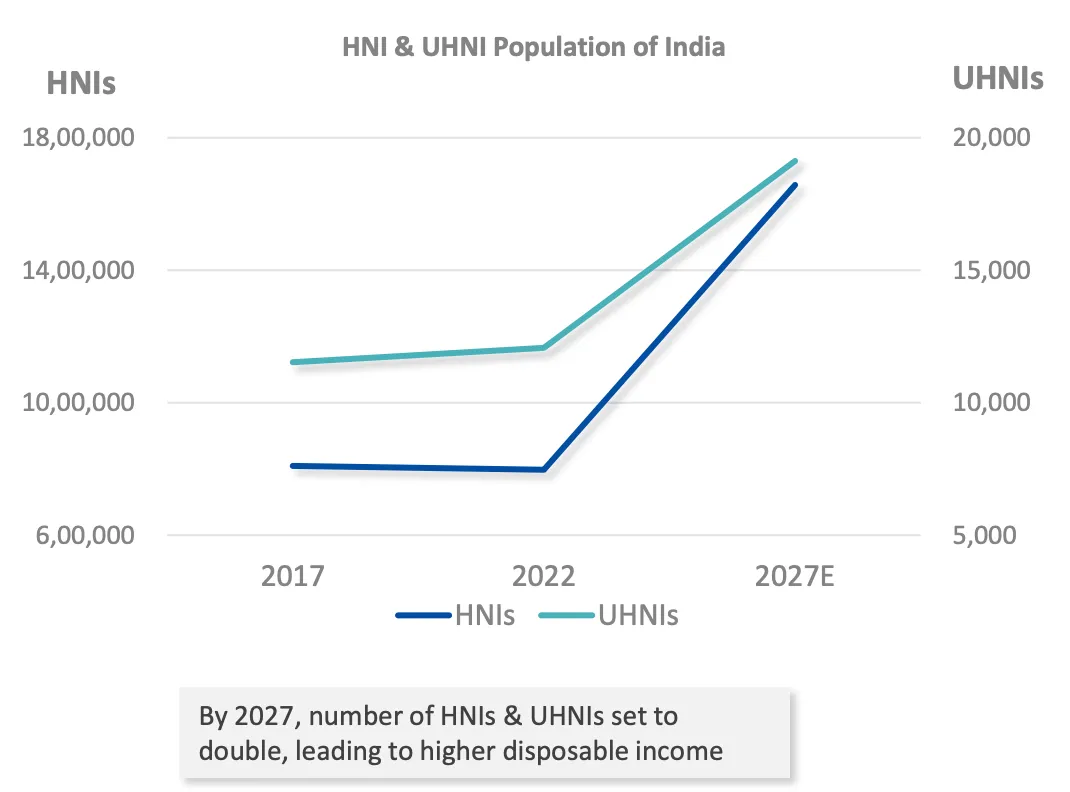

Increasing Number of HH with Surplus Income

- The distribution of household wealth in India has undergone significant changes over the past few decades. Going forward, the total HH financial assets are expected to touch INR 275.5 billion by 2027.

- Specifically within income distribution, the number of individuals earning more than INR 1Cr in annual income have grown at a CAGR of 15% (1.8X vs overall tax filers) from FY18 to FY23 and are expected to touch 3.4L by FY27.

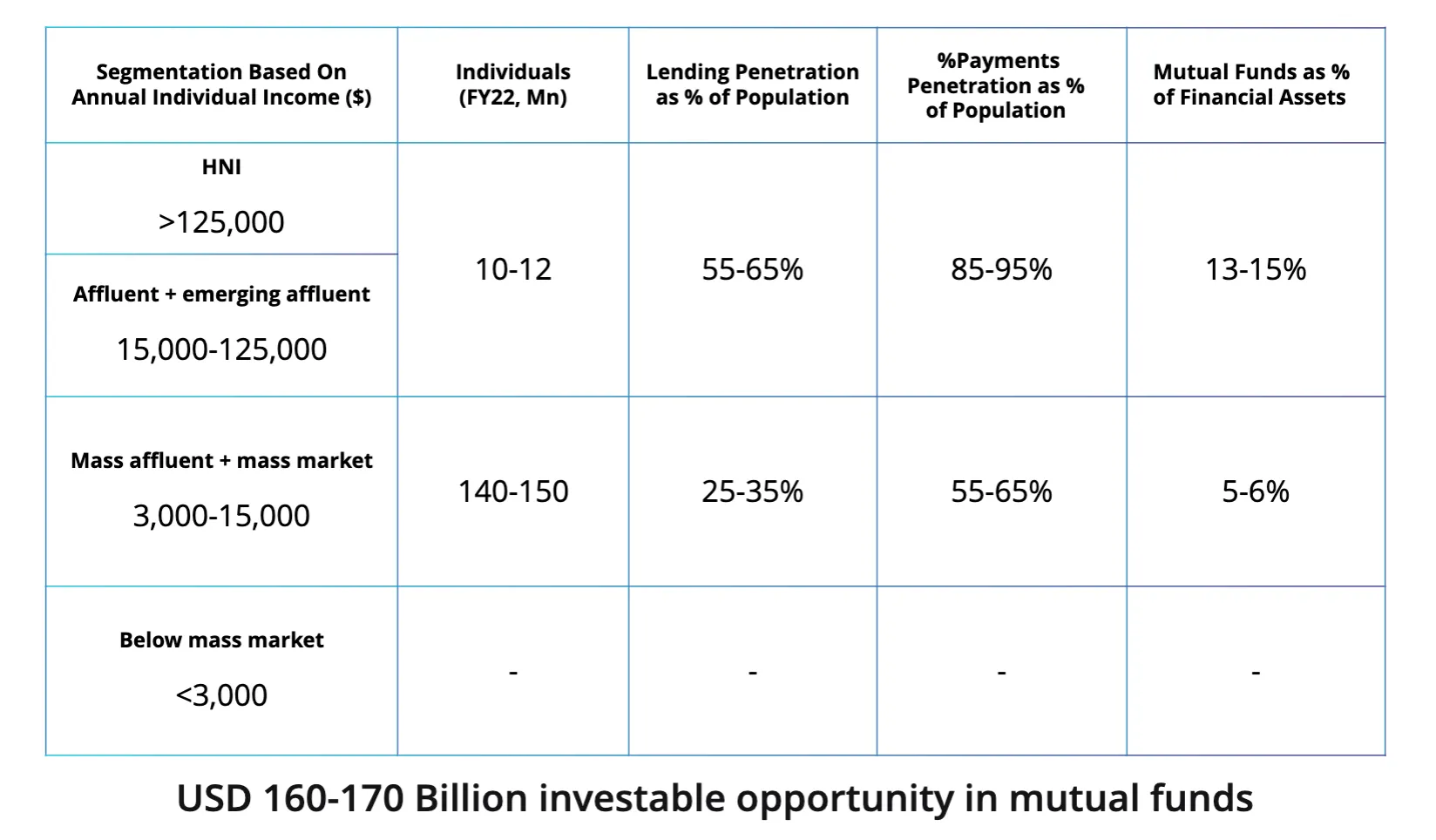

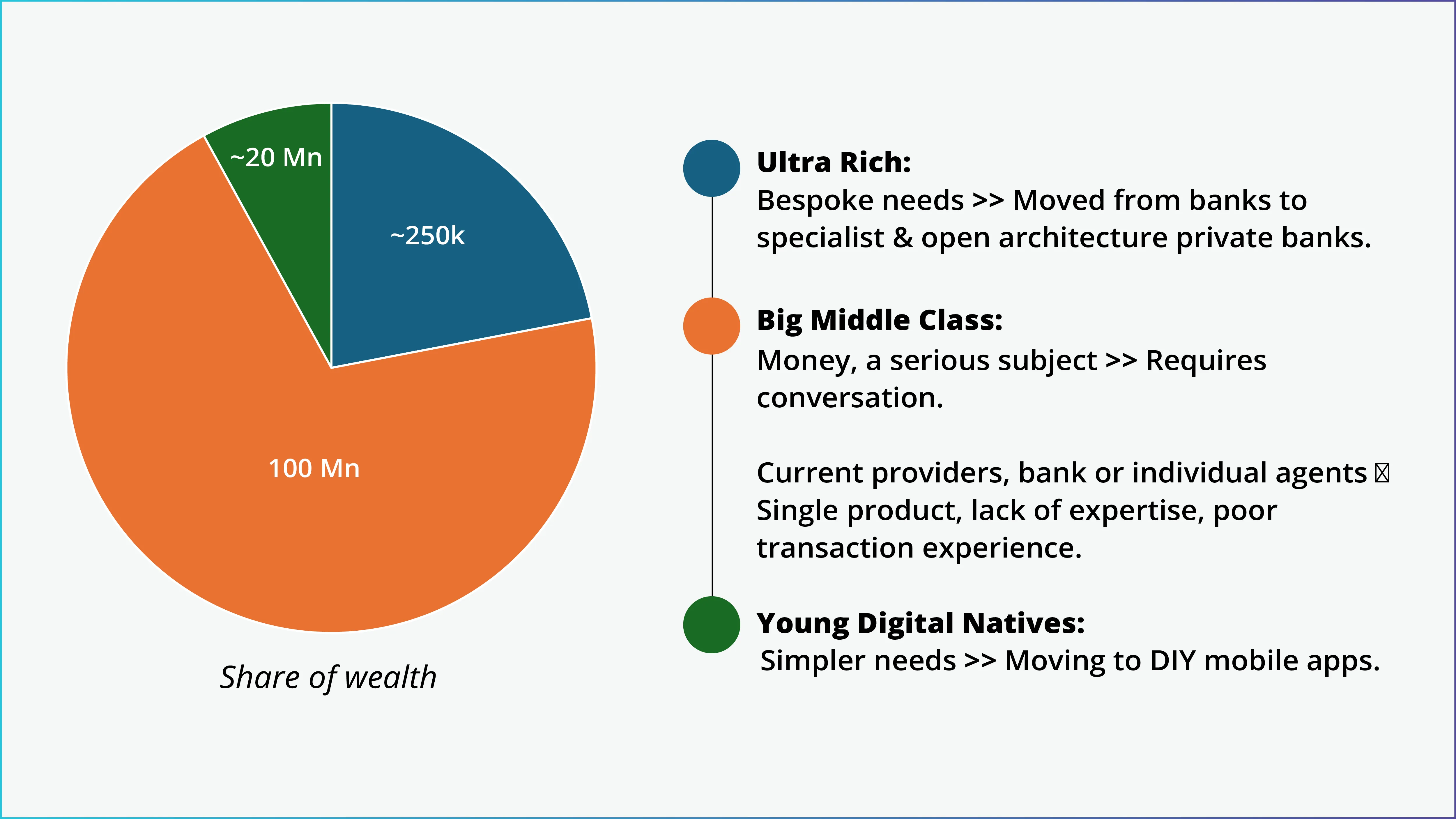

- Another interesting segment is the missing middle: mass affluent and mass market investor, earning between INR 2.5L to INR 13L, where the penetration of mutual funds (as a % of financial assets) still remains very low at 5-6%.

Market Buoyancy and Investor Confidence Driven by Confidence in Earnings and GDP Growth

- India's current economic expansion resembles the 2003-07 boom period driven by rising investment as a percentage of GDP. After a decade of decline, the investment-to-GDP ratio is rising again, now at 34% and expected to reach 36% by FY2027, led initially by public capex spending. In 2003-07, private investment outpaced consumption, fueling productivity, jobs and income growth. Public investment lagged then, constraining infrastructure. Now, there are early signs of a private capex uptick as corporate profits improve, though private consumption remains relatively weak compared to pre-pandemic levels. The capex cycle is seen as a key growth driver currently, similar to 2003-07 when GDP growth averaged 8.6%.

.webp)

Equities and gold have driven a strong increase in wealth in India over the past 4 years. India’s market cap has increased over 80% over the past 3 years with rising retail participation. Gold price also rose 65% over 2020-23. In terms of market cap, the Indian equity market has just overtaken Hong Kong and ranks 4th, led by US, China, and Japan and has a long runway of growth ahead.

Diverse Investor Profiles

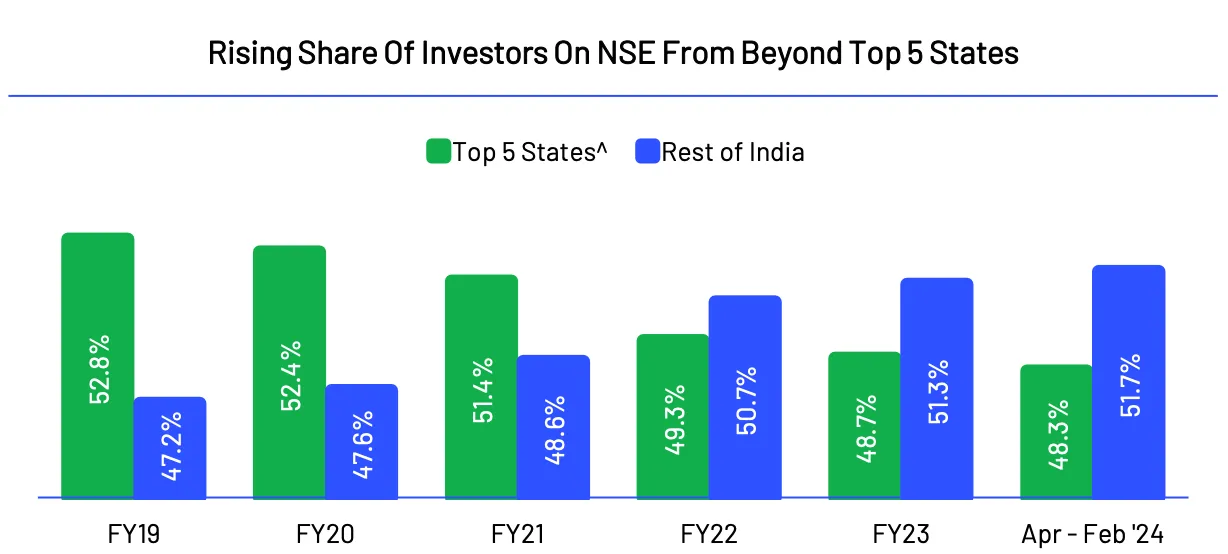

India is now seeing a decentralisation of investment activity, highlighting growing financial inclusivity and market penetration in the broader regions of India. Public data indicates a broadening investor base across the country, with more individuals from beyond the major states participating in the NSE. The trend suggests In FY19, the share of investors from the top five states was 52.8%, while the rest of India accounted for 47.2%. This trend shifts gradually, with the top five states' share declining to 48.3% by FY23 and further to 48.3% by April-February 2024, while the rest of India sees a corresponding increase to 51.7% in the same period.

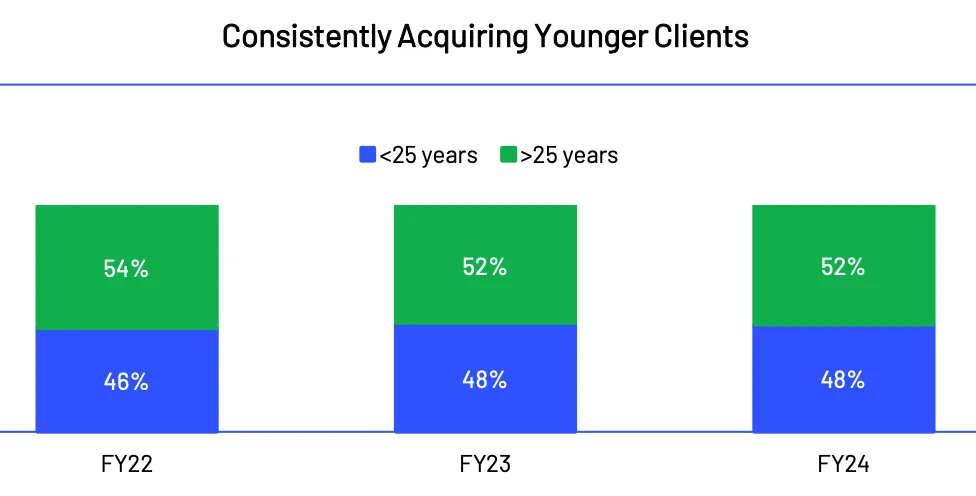

For AngelOne, in FY22, 46% of the clients were under 25 years old, while 54% were over 25 years old. Moving to FY23, there is a notable increase in the younger client segment, rising to 48%, while the proportion of clients over 25 years drops to 52%. This upward trend for younger clients stabilizes in FY24, with the younger segment maintaining a 48% share and the older segment at 52%. This consistent increase in the percentage of younger clients indicates a significant shift towards engaging a younger demographic, reflecting a broader trend in the financial market. It suggests that younger investors are becoming more prominent and influential, potentially driven by increased financial literacy, accessibility to investment platforms, and targeted strategies by financial institutions to appeal to younger audiences.

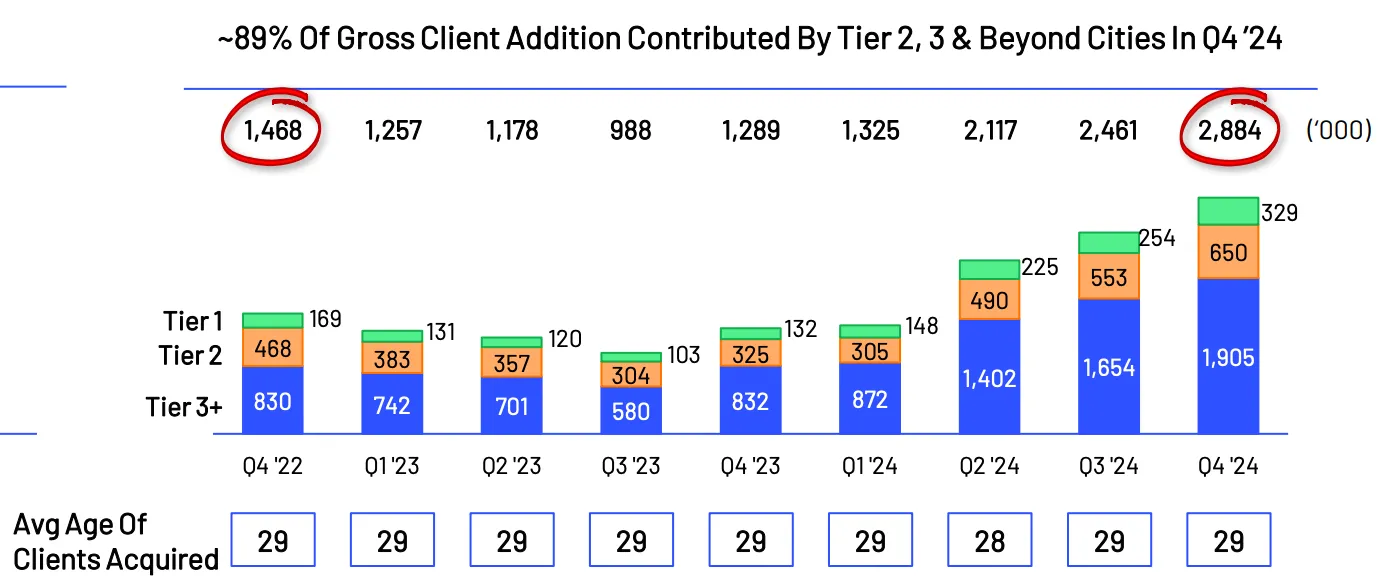

For AngelOne, 89% of new client acquisition can be attributed to T2+ cities. Additionally, the average age of clients has consistently remained below 30. This trend reflects the growing importance and untapped potential of smaller cities in the financial market, showcasing a broader movement towards financial inclusivity and market expansion in diverse regions.

Future Outlook for Asset Classes

Projected GDP per Capita Growth and Its Impact on Surplus Capital and Yield-Seeking Investments

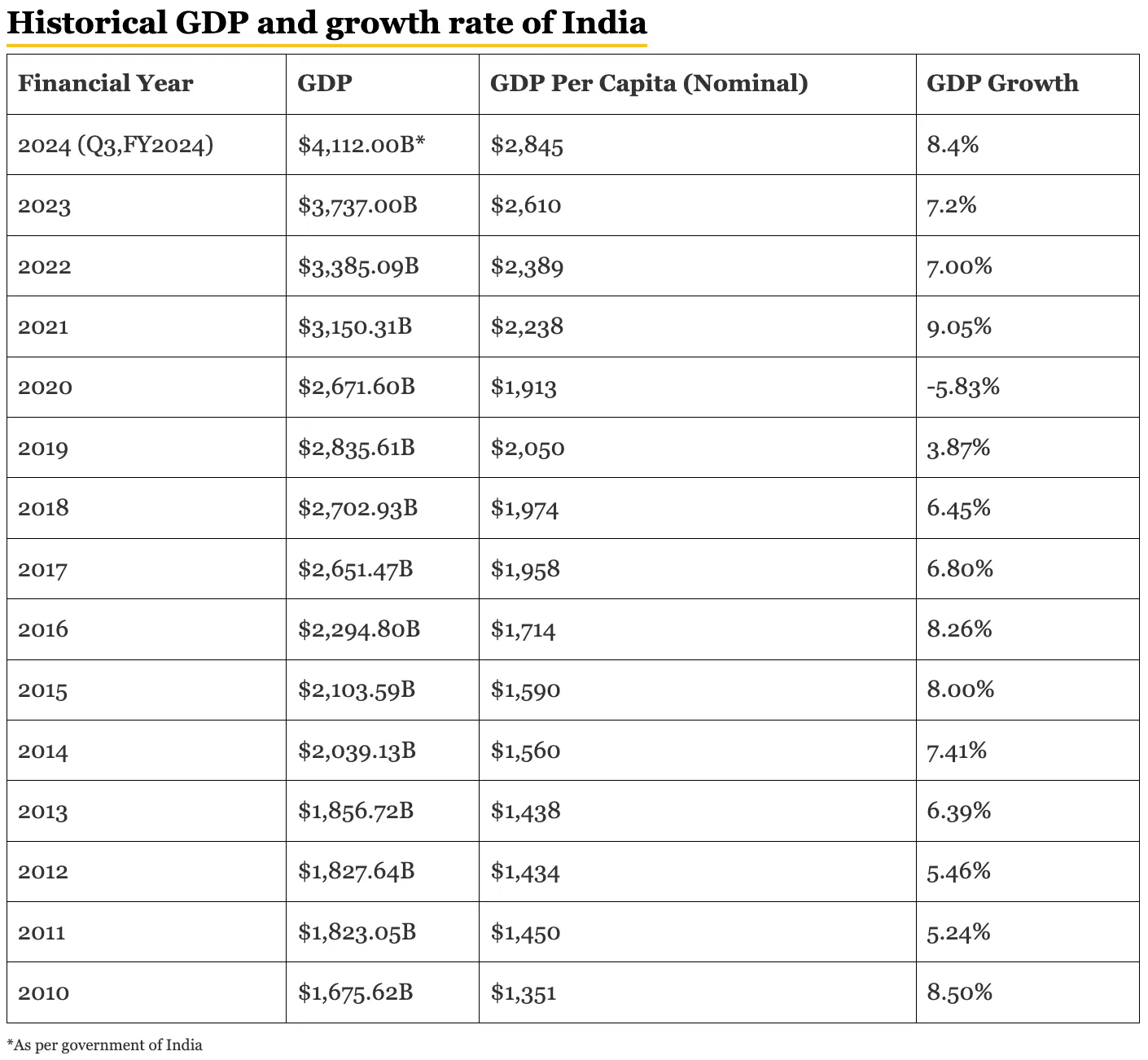

The projected GDP per capita for India in 2030 is expected to reach approximately $4,000. This significant increase from the current per capita ($2,845) income is driven by robust growth factors such as external trade, which is anticipated to nearly double, and substantial household consumption - signalling a robust economic expansion.

As incomes grow, individuals will have more disposable income, leading to increased available capital for investments. This trend is expected to stimulate yield-seeking investments, driving market diversification and financial inclusion across the country. With the rise in surplus income, there is a noticeable shift towards equity investments, which offer high rewards. Indians are becoming more proactive about risk mitigation while aiming to harness the long-term benefits of equity investing. It is projected that equity will account for 10% of total household assets by 2033.

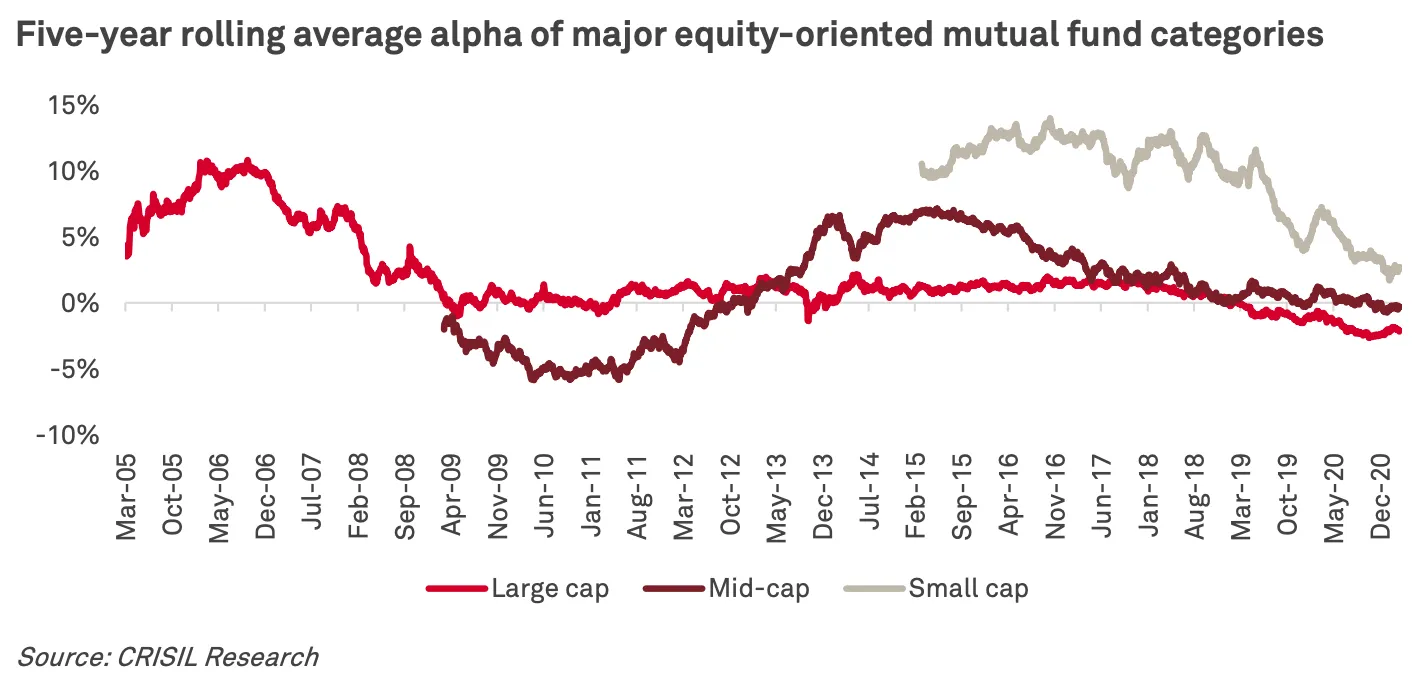

Broader Shift Towards Passive Products as Market Alpha Shrinks

The Indian mutual funds industry is experiencing a significant shift towards passive fund management - passive fund assets have surged nearly five times in the past five years, primarily driven by large institutional investors like provident fund trusts. As of 2020, passive funds accounted for approximately 31% of global mutual fund assets. In India, this growth has been further bolstered by the government’s use of exchange-traded funds (ETFs) for public sector enterprise divestment. Concurrently, actively managed funds are underperforming, particularly in the large-cap segment where nearly 90% of funds generated negative alpha in recent years.

This underperformance is attributed to increased market efficiency, regulatory constraints, and the inability of fund managers to replicate index weights for top-performing stocks. As a result, more investors and financial advisors are turning to passive funds for their portfolios.

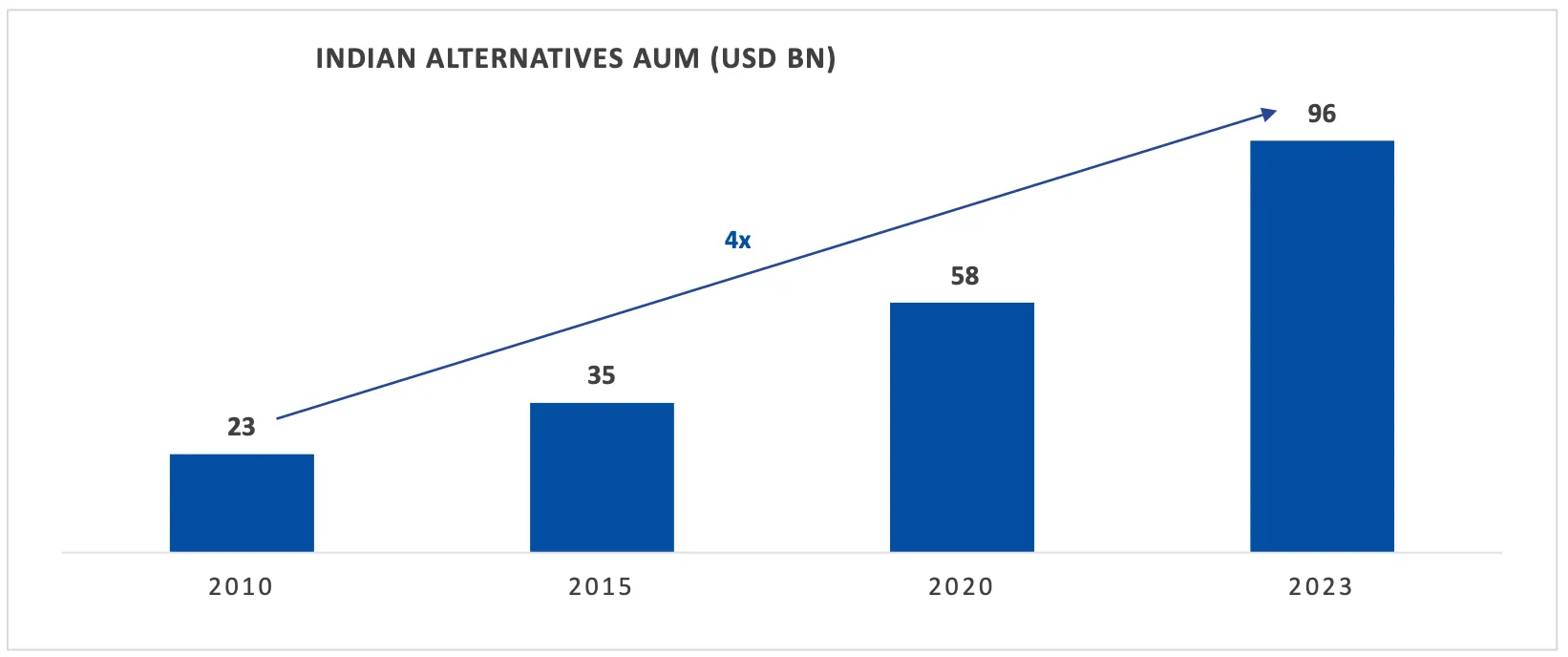

Growth Potential in Alternative Asset Industries

The asset management industry is expected to face consistent volatility, a high-interest rate regime, and low growth in the near term, necessitating a pivot towards alternative investment approaches for sustained growth and effective risk-reward. The alternative investment industry is projected to witness a CAGR of 9.3% between 2021 and 2027. Globally, private credit strategies offering higher rates are anticipated to drive this growth, with increased focus on hedge fund strategies capitalizing on volatility. Private equity and REITs will remain attractive but will face challenges due to higher interest rates and lower growth, resulting in strong competition for appealing opportunities.

As India’s GDP scales up to USD 10 trillion over next 10-11 years, Alternative Asset Management AUMs estimated to grow exponentially to USD 600 billion. This projection is driven by the increasing diversification of investment portfolios by HNIs and UHNIs in India. These investors are increasingly allocating a larger portion of their wealth to alternative asset classes such as private equity, venture capital, real estate, and hedge funds. This trend reflects a broader shift towards more sophisticated and diversified investment strategies in the Indian financial market.

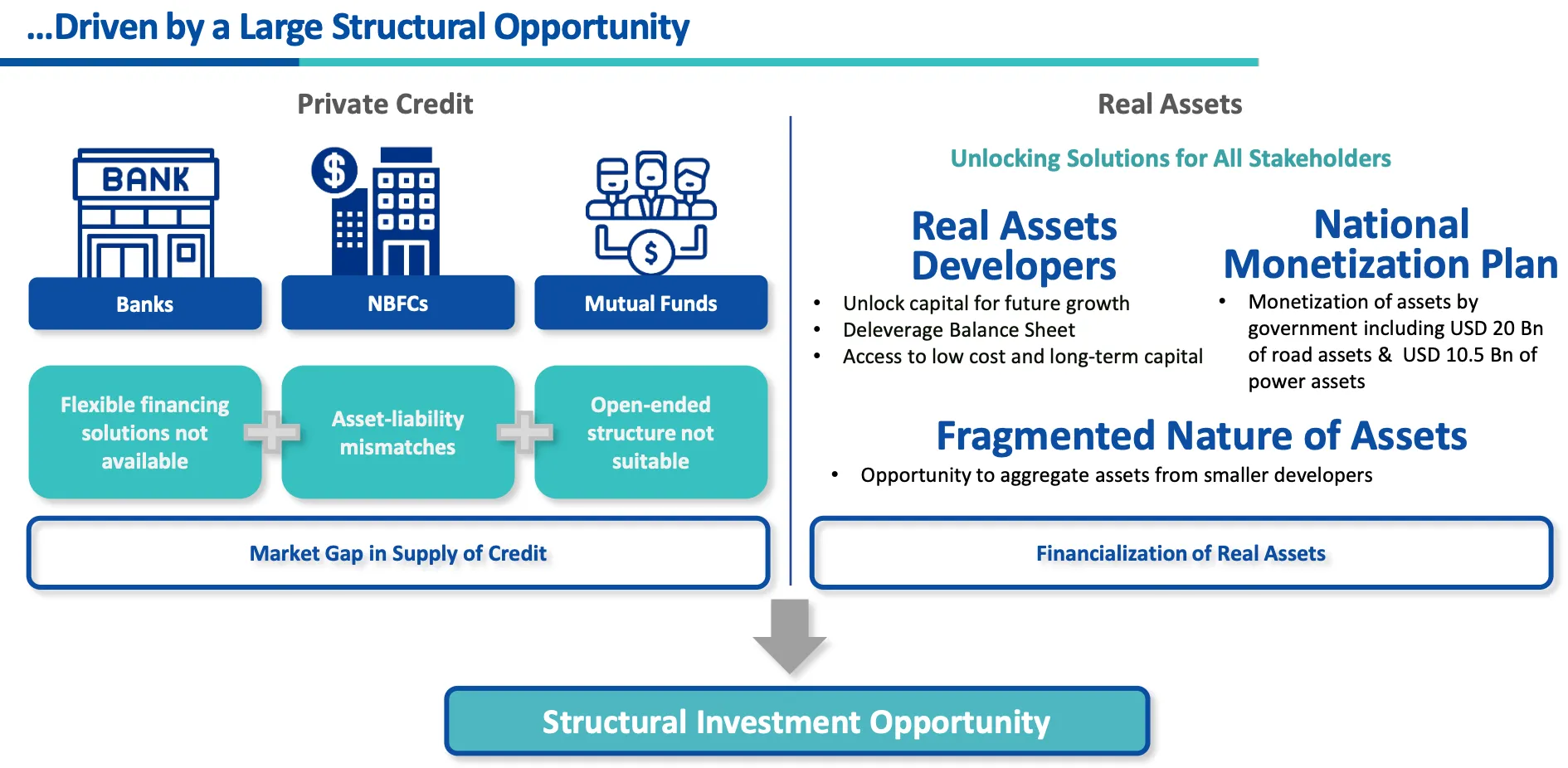

In alternative assets, there is a significant structural investment opportunity driven by gaps in the supply of credit and the potential for real asset development. The private credit sector, including banks, NBFCs, and mutual funds, faces challenges such as the unavailability of flexible financing solutions, asset-liability mismatches, and unsuitable open-ended structures. This creates a market gap in the supply of credit. In the realm of real assets, unlocking capital for future growth, deleveraging balance sheets, and accessing low-cost, long-term capital are key benefits for real asset developers. The National Monetisation Plan includes the monetisation of USD 20 billion in road assets and USD 10.5 billion in power assets by the government. Additionally, the fragmented nature of assets presents an opportunity to aggregate assets from smaller developers. Overall, this scenario sets the stage for substantial structural investment opportunities, particularly through the financialisation of real assets.

Opportunities for Financial Services Startups

Serving the Emerging, Aspirational Market Segment with Wealth Creation Solutions

India presents a significant market opportunity for building new financial services distribution companies. The emerging, aspirational market segment, although not yet financially literate, is aspirational about creating wealth. This segment of the population has significant investable surplus but faces some challenges:

- Finding suitable products and solutions that align with their specific needs and value systems

- Lack of financial literacy and trusted advisors

- Fear of market volatility and high minimum investment options in physical assets

Historically, solutions for these audiences have primarily been limited to term deposits from banks and chit funds - sold via bank or individual agents that offer limited products, lack expertise and have high friction processes to build investing habits. Hence, there is an opportunity to serve this audience through a platform that facilitates saving and investing by offering low-risk, highly-liquid investment schemes. These schemes should be easy to understand, providing stable investment returns through assets with small ticket sizes to start with. This approach ensures that even novice investors can confidently participate in financial markets, gradually building their investment portfolios with minimal risk.

Omni-Financial Advisors: Leveraging Technology to Cater to the Aspirational

Much has been said about robo-advisory and personalized asset allocation platforms, highlighting their potential to revolutionize the financial advisory landscape. We believe that the aspirational segment, in particular, could greatly benefit from a more digitized version of IFAs and wealth advisors because this solves for reach. These digital advisors provide tailored financial guidance, helping users make informed decisions and stay invested in the long term. Advisors coupled with digital solutions also promote better financial habits by providing continuous monitoring and regular updates on investment performance. They can send alerts and reminders to encourage users to stay on track with their investment plans, make necessary adjustments, and take advantage of new opportunities as they arise.

.webp)

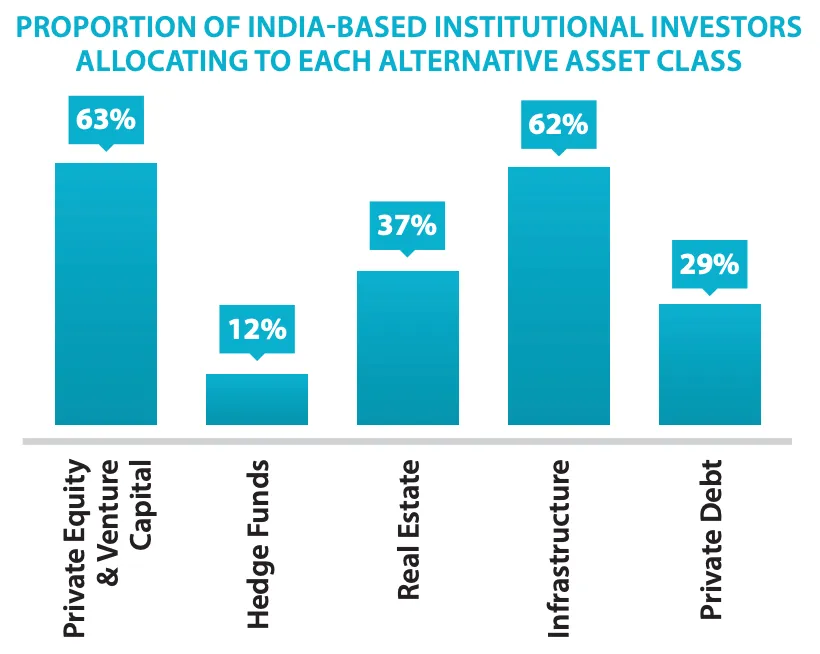

Broader Access to Alternative Assets for Diversification and Higher Returns

The alternative assets market, though not as pervasive, offers potential customers the ability to diversify into riskier assets with higher potential returns or into assets uncorrelated with their other investments. However, access to alternative investments has been largely restricted to the wealthiest households in India.

Alternative assets present a promising avenue for diversification and higher returns, significant barriers still limit their widespread adoption in India: the illiquidity of investments, high minimum investment thresholds, regulatory complexity, and a lack of client education. As the market moves towards greater financialisation, there is an increasing trend towards digital disintermediation within the value chain and higher returns from yield-bearing assets.

Hence, there is an opportunity for a multi-asset platform that has the potential to significantly disrupt the market and drive higher adoption for asset classes across risk and return profiles.

Conclusion

The transformation of India’s wealth landscape presents a substantial opportunity for financial services startups. By serving the emerging, aspirational market segment with wealth creation solutions, leveraging technology for personalised financial guidance, and providing broader access to alternative assets, startups can significantly disrupt the market.

Trust-based multi-asset distribution models can address existing barriers such as illiquidity, high minimum thresholds, regulatory complexity, and lack of client education, making alternative investments accessible to a broader audience.

As the market moves towards greater financialisation, digital disintermediation, and higher returns from yield-bearing assets, the potential for growth in the alternative asset industry is immense. Financial services companies that can innovate and cater to the evolving needs of Indian investors stand to benefit from this transformative phase, driving both financial inclusivity and sustained wealth creation in India.

DISCLAIMER

The views expressed herein are those of the author as of the publication date and are subject to change without notice. Neither the author nor any of the entities under the 3one4 Capital Group have any obligation to update the content. This publications are for informational and educational purposes only and should not be construed as providing any advisory service (including financial, regulatory, or legal). It does not constitute an offer to sell or a solicitation to buy any securities or related financial instruments in any jurisdiction. Readers should perform their own due diligence and consult with relevant advisors before taking any decisions. Any reliance on the information herein is at the reader's own risk, and 3one4 Capital Group assumes no liability for any such reliance.Certain information is based on third-party sources believed to be reliable, but neither the author nor 3one4 Capital Group guarantees its accuracy, recency or completeness. There has been no independent verification of such information or the assumptions on which such information is based, unless expressly mentioned otherwise. References to specific companies, securities, or investment strategies are not endorsements. Unauthorized reproduction, distribution, or use of this document, in whole or in part, is prohibited without prior written consent from the author and/or the 3one4 Capital Group.